When you borrow money, you are simultaneously entering into a contractual agreement. Failing to fulfill your payment obligations can lead to various repercussions, including legal consequences. Discover further information about the potential outcomes of missing installment loan payments below, and obtain guidance on actions to consider if a loan is placing an excessive financial burden on you.

What Happens When You Default on an Installment Loan?

Failing to make a loan payment typically results in penalties, and the severity of these consequences increases with the length of the delay. The specific measures taken in response to a missed payment depend on the lender’s policies and the terms of your agreement.

The primary objective should be to prevent delinquency. Delinquency occurs when you fall behind on loan payments and can potentially lead to default. Once you miss a payment, you become delinquent on the loan. The following are common repercussions associated with different degrees of delinquency when it comes to installment loans.

What Happens if You Miss a Payment on an Installment Loan?

In the event of a slight delay in making a loan payment, there is a possibility of having a grace period. This means that if your loan agreement includes a grace period, typically within 10 days, your payments will not be officially classified as late as long as they are made within that designated timeframe following the due date. However, the duration and conditions of a grace period vary depending on your specific lender and loan agreement, so it is important to carefully review all the details. It’s worth noting that not all loans or accounts offer a grace period, and it is intended to serve as a safety net for occasional instances when you forget or face difficulties making a payment, rather than permanently shifting your due date.

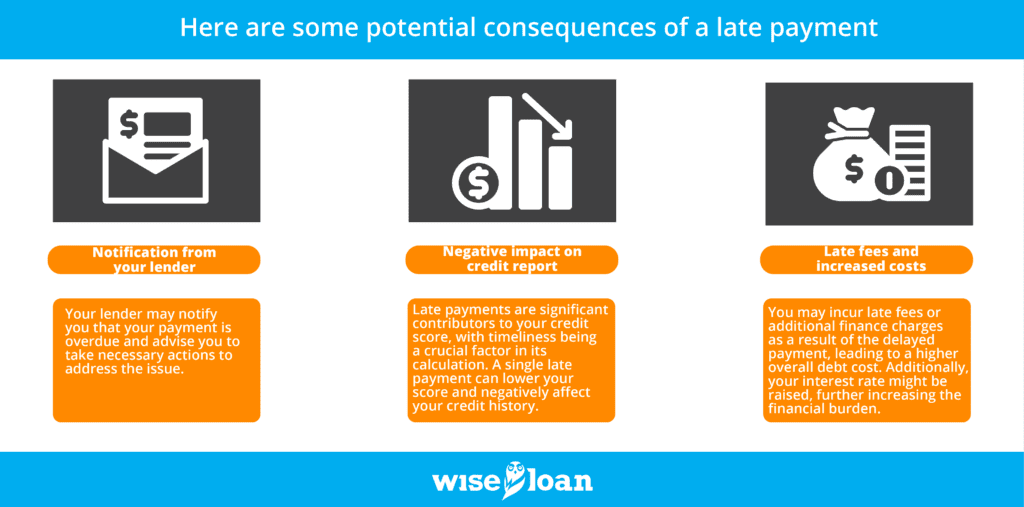

If you exceed the grace period or your loan does not have one, your payment will be considered late. Here are some potential consequences:

- Notification from your lender: Your lender may notify you that your payment is overdue and advise you to take necessary actions to address the issue.

- Negative impact on credit report: Late payments are significant contributors to your credit score, with timeliness being a crucial factor in its calculation. A single late payment can lower your score and negatively affect your credit history.

- Late fees and increased costs: You may incur late fees or additional finance charges as a result of the delayed payment, leading to a higher overall debt cost. Additionally, your interest rate might be raised, further increasing the financial burden.

Missing Multiple Loan Payments:

If you miss two or more consecutive payments, the consequences can become more severe. Late fees and finance charges may accumulate further, and the lender may report these additional instances of tardiness to the credit bureaus. Being 60 or 90 days late, or beyond, generally has a more detrimental impact on your credit than a single missed payment.

At a certain point, if you continue to miss payments for an extended period, the lender may declare your loan to be in default. The specific timeframe for default varies among lenders, but it commonly occurs after 90 days or more of consecutive missed payments.

What Can a Loan Company Do if You Don’t Pay?

In the event of default, the lender has the option to transfer your account to collections. Initially, some lenders may initiate an internal collections process, where they become more assertive in their efforts to recover the outstanding debt. This may involve sending you notices regarding the amount due and informing you that failure to pay within a specific timeframe will result in further collections activities.

Certain lenders may opt to outsource defaulted accounts to external collection agencies. These agencies are responsible for pursuing debt repayment, which could include taking legal action against you and seeking a judgment. If successful, they may have the authority to garnish your wages or place liens on your accounts.

It’s essential to understand that as the borrower, you have rights during this process, as outlined by the Fair Debt Collection Practices Act. When dealing with debt collectors, it is crucial to familiarize yourself with your rights to ensure you can safeguard your interests.

What Can Cause You to Miss a Loan Payment?

Many individuals who find themselves missing loan payments often do so with good intentions. It is a common occurrence in life and does not necessarily indicate poor money management skills. Oftentimes, unforeseen circumstances arise that contribute to missed payments. Some frequent reasons for missing loan payments include:

- Oversight due to competing obligations and distractions.

- Misunderstanding the loan terms or requirements, leading to a lack of awareness regarding the payment due date.

- Financial difficulties and temporary inability to meet the loan payment obligations.

While these reasons are understandable and can be considered mistakes, it is important to recognize that missing loan payments still carry consequences. Therefore, it is advisable to take proactive measures to avoid such situations and alleviate the financial strain associated with loan payments.

Tips for Making Your Installment Payments on Time

Maintaining a well-planned and organized approach is crucial to adhering to your payment plan. To ensure your ability to make loan payments, it is essential to have a realistic understanding of how much you can afford to borrow. Consider your income, existing bill payments, and necessary expenses like groceries and fuel. If there are insufficient remaining funds to cover a loan payment, it may be necessary to wait until you can reduce expenses, increase your income, or obtain a more favorable interest rate.

Once you determine that an installment loan is within your budget, implementing organizational measures becomes essential to ensure consistent and timely payments. Creating a written budget and faithfully following it can help effectively manage your finances each month. Utilize calendars, planners, or smartphone apps with reminders to stay on top of payment due dates and avoid forgetting to make the necessary payments.

Many lenders offer the convenience of automatic payments (ACH), allowing you to set up payments directly from your checking account on designated dates. Auto-payments serve as an excellent tool to prevent missed payments, but it remains important to maintain organization and ensure sufficient funds are available in your checking account on the designated day.

What to Do if You Can’t Pay Your Installment Loan

If you find yourself unable to make a loan payment, it is important not to disregard the issue. Take immediate action and contact your lender to inform them about your situation and the reasons behind your inability to make the payment. This could include factors like job loss or a significant change in income.

Many lenders offer assistance programs specifically designed for such circumstances. Even if your lender doesn’t have a formal program, it is still crucial to explore all available options. Having a comprehensive understanding of your alternatives will enable you to make informed decisions and devise a plan for managing your debt effectively.

In certain situations, you might even qualify for a short-term loan to address temporary financial challenges. By working with responsible lenders like Wise Loan, you can apply for a loan that provides instant, same-day, or next-day funding if approved. Discover more information and submit an application for an installment loan from Wise Loan today.

FAQs About Installment Loans

How can I terminate an installment loan?

The most effective approach to concluding an is to fully repay it. While discharging certain loans through bankruptcy is a possibility, it can have significant repercussions on your overall financial well-being and credit standing. Exploring options such as negotiating with the lender for an extended payment period or refinancing at a lower interest rate could help alleviate the financial burden associated with the loan.

Can I be arrested for failing to pay a loan?

No, non-payment of debts does not lead to arrest. However, debt collectors have legal means to ensure repayment, such as wage garnishment.

Will loan extensions impact my credit score?

Loan extensions typically do not have a direct impact on your credit score. They can be a beneficial strategy for managing payments and avoiding missed payments, which could negatively affect your credit rating.

The recommendations contained in this article are designed for informational purposes only. Essential Lending DBA Wise Loan does not guarantee the accuracy of the information provided in this article; is not responsible for any errors, omissions, or misrepresentations; and is not responsible for the consequences of any decisions or actions taken as a result of the information provided above.

More information on Installment Loans and how they work in your state: