Credit scores can be both simple and incredibly complex. Maintaining a good or excellent credit score requires effort, but understanding the factors that can impact your score empowers you to make informed financial decisions tailored to your personal situation. This knowledge can make a significant difference when seeking loans or other forms of financing. Below is a comprehensive guide outlining everything that can influence your credit score.

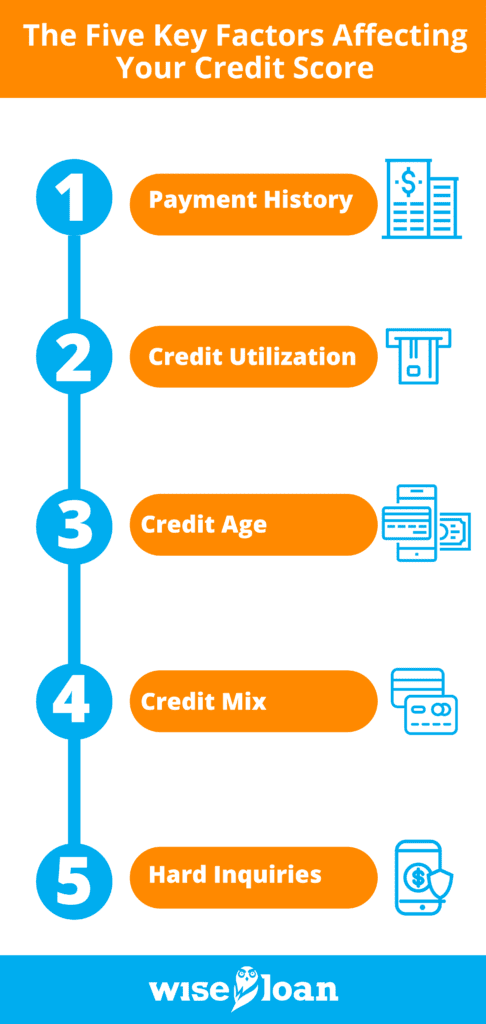

The Five Key Factors Affecting Your Credit Score

Your credit score comprises five major components. Various actions, statuses, and reported items within these categories can either increase or decrease your score. Familiarizing yourself with these factors is crucial in understanding how your credit score may be affected and how you can rectify it if necessary.

- Payment History

Timely bill payments demonstrate your responsibility and ability to repay debts as agreed. Your payment history is a significant factor in determining your credit score. This is why making purchases such as a car on credit can have a positive long-term impact on your credit score, provided you make payments on time.

- Credit Utilization

Credit utilization refers to the amount of credit you are currently using. This factor is most relevant to revolving credit accounts, such as credit cards or lines of credit. Your credit utilization ratio is calculated by comparing your outstanding balance to your credit limit.

Maxing out your credit cards and lines of credit signals to lenders that you may be a risky borrower. High credit utilization suggests a lack of control over your personal finances and may lead to increased monthly payments, elevating the risk of defaulting on loans. Consequently, credit utilization is almost as significant as payment history in determining credit scores. If you are utilizing credit cards to build credit, it is essential to keep your balances low.

- Credit Age

Credit age refers to the length of time you have held a credit history and the average age of your open accounts. If you have no credit history or are relatively new to credit, your credit score may be negatively affected. Without accounts that are at least six months old, you may not have a credit score at all.

- Credit Mix

Credit mix entails having a diverse range of credit types. Lenders prefer to see that you can effectively manage both installment and revolving credit. If you solely have a personal loan or only possess a credit card, your credit mix may be considered inadequate, which can harm your credit score.

- Hard Inquiries

When someone requests your credit information to evaluate you for credit, it results in a hard inquiry appearing on your credit report. Each hard inquiry slightly lowers your credit score, so having too many within a short time frame can be detrimental.

Why You Have Multiple Credit Scores

It is possible to have both a good and a bad credit score simultaneously because most individuals have multiple credit scores. This occurs due to several factors:

Firstly, there are multiple credit bureaus, namely TransUnion, Equifax, and Experian. These bureaus do not share information provided by lenders and other entities, and not all lenders report to all three bureaus. As a result, the information within your credit file can differ across bureaus. For example, you may have a late payment reported to one bureau but not the others.

Secondly, there are various credit score models, which are algorithms that calculate your credit score based on the information in your credit profile with the bureaus. Applying the same credit score model to information from each bureau can yield three different credit scores. The number of potential credit scores a person can have depends on the entity pulling the score, the bureau’s information used, and the scoring model employed.

A Comprehensive Checklist of Credit Score Influencers

Credit scores fluctuate based on various factors. Understanding these factors helps you build credit and avoid actions, whenever possible, that may reduce your score. Below is a complete checklist of elements that can positively or negatively impact your credit:

Positive Factors:

– On-Time Payments: Consistently paying your bills on time helps increase your credit score. However, it’s important to note that some creditors, like landlords or utility and insurance companies, may not report payments to credit bureaus. To build credit without installment loans or credit cards, you can utilize services like Experian Boost, which add utility bills and other payments to your credit report.

Negative Factors:

– Late Payments: Late payments are typically reported by lenders to one or more credit bureaus, and they have a negative impact on your score. The frequency and lateness of the payments exacerbate this impact.

– Default or Collections Accounts: If you default on a loan or account, leading to it being sent to collections, it is reported to the credit bureaus. Even if the account was not initially reported, it will appear on your credit report once it enters collections. Defaults and collections accounts significantly harm your credit score.

– Paying or Settling Collections Accounts: The impact of paying or settling collections accounts on your credit score depends on the scoring model. In some cases, it may have little to no impact on your score. However, paying or settling such accounts can be viewed positively by lenders, and some may require you to address old accounts before approving a mortgage, for instance.

– Maintaining a High Credit Card Balance: Carrying a high balance on revolving credit accounts negatively affects your credit score by increasing your credit utilization ratio. It is recommended to keep your total credit utilization ratio below 30% by not exceeding $300 in balance for every $1,000 in credit limit.

– Paying Down Debt: Paying down debt, especially revolving credit debt, usually has a positive impact on your credit score. Consolidating credit card debt to facilitate repayment can also be beneficial, but caution should be exercised when opening new loans and closing old ones during the debt repayment process.

– Closing Old Accounts: Closing old accounts can have a negative impact on your credit score as it reduces the overall age of your credit. It is important to consider the average age of your credit when deciding to close accounts.

– Opening New Accounts: Opening new accounts can affect your credit score in multiple ways. It can decrease the average age of your credit, involve a hard inquiry, and increase your total debt. These factors may have a negative impact on your credit score. However, maintaining timely payments on new accounts can contribute positively to your credit score over time.

– Applying for Credit: Simply applying for credit can impact your credit score. When a lender performs a hard pull on your credit report to evaluate you for a loan or account, it is recorded and can slightly reduce your score. Multiple hard inquiries within a short period can further lower your score and give the impression that you are desperate for credit, which is viewed negatively by lenders. Hard inquiries remain on your credit report for two years but do not have the same impact on your score throughout that time.

– Foreclosures or Repossessions: Foreclosures and repossessions have significant negative impacts on your credit scores. These events suggest that you were severely delinquent on a loan, leading to the seizure of the property securing the loan.

– Bankruptcies: Bankruptcies are major negative items on your credit report. Although the impact on your score may not be substantial, as individuals filing for bankruptcy typically have many late payments, potential foreclosures, or collection accounts, it can still have long-lasting effects. Bankruptcies remain on your credit report for up to 10 years from the filing date.

– Activity on a Loan You Cosigned: If you cosign a loan or credit opportunity for someone else, their management of the account may impact your credit. Many lenders report payments and account information to the credit files of cosigners. Late payments or defaults on the loan can negatively affect your credit score.

– Being an Authorized User on Someone’s Credit Card Account: Being added as an authorized user to another person’s credit card account can potentially boost your credit score quickly. However, if the primary account holder accumulates a high credit card balance or is late with payments, your credit score may be negatively impacted.

– Mistakes/Incorrect Information: Approximately 20% of people discover errors on their credit reports. Inaccurate negative information, such as late payments or defaults on loans that do not belong to you, can harm your credit score. Fortunately, you have the right to a fair and accurate credit report. If you identify errors, you can request the relevant credit bureau to investigate and make corrections by submitting a written request.

– Time: The passage of time plays a significant role in your credit score. Most negative items age off after approximately 7.5 years, ceasing to impact your score. Additionally, negative items have a diminishing impact over time. Understanding this aspect allows you to work towards building a more positive credit score in the future.

Comprehending loans and credit is vital for everyone. Whether you are currently seeking a personal loan or simply aiming to maintain a healthy credit score, understanding the factors that influence it is the first step. Contact us to learn more about our responsible lending approach. Applying for a loan is a quick process, taking only minutes, and depending on your bank, you can receive the funds as soon as the next business day.

The recommendations contained in this article are designed for informational purposes only. Essential Lending DBA Wise Loan does not guarantee the accuracy of the information provided in this article; is not responsible for any errors, omissions, or misrepresentations; and is not responsible for the consequences of any decisions or actions taken as a result of the information provided above.