In brief, a loan falls under the category of credit, but not all forms of credit are classified as loans. To comprehend the distinction between a loan and credit, it’s essential to understand the various meanings of the term “credit.”

Credit can have multiple interpretations. For instance, in the context of this article, credit can refer to two specific things:

- Financial standing: This aspect of credit pertains to how you are perceived as a consumer and borrower. A higher credit score indicates a more favorable perception, increasing the likelihood of lenders or others being willing to work with you.

- Monetary credit to you: In accounting terms, credit is recorded as a positive or income entry. When your account is credited, money is added to the total amount accessible to you. When a lender agrees to provide you with money – whether through a loan, credit card, or any other format – it enhances your available funds, allowing you to make purchases that need to be repaid later.

So, what exactly is a loan?

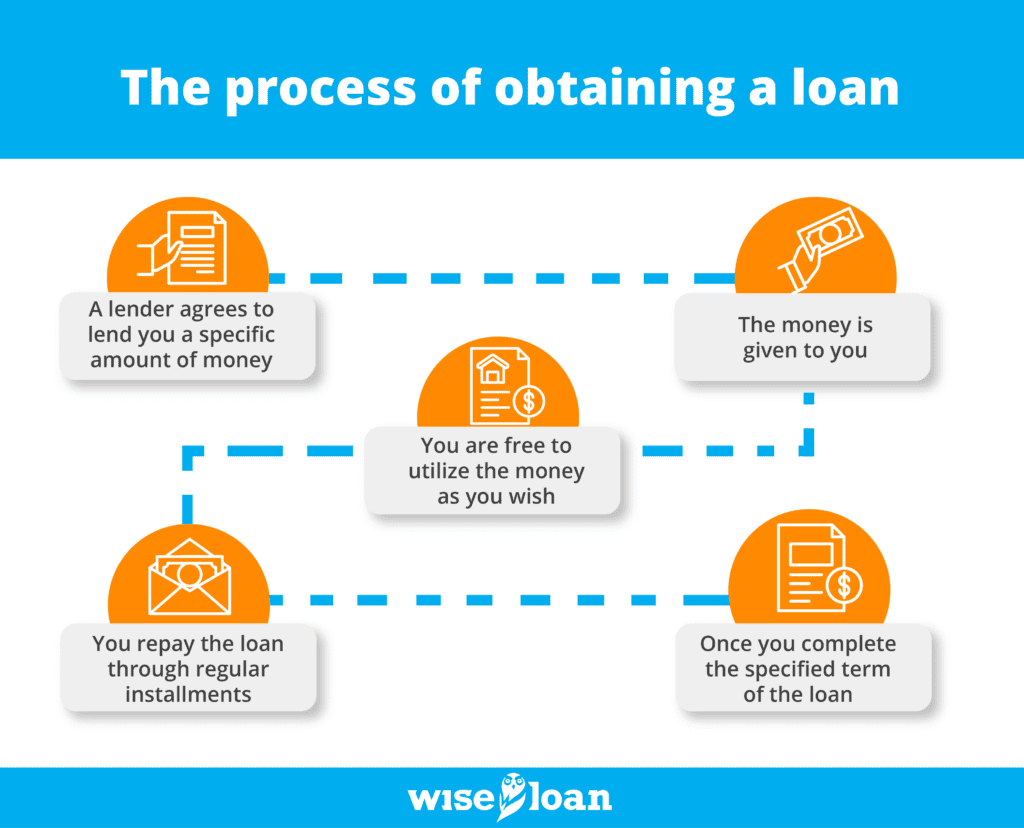

A loan is a particular form of credit; it is considered a type of installment credit and involves a contractual agreement. Generally, the process of obtaining a loan works as follows:

- A lender agrees to lend you a specific amount of money, and in return, you commit to paying back the money over time, along with an agreed-upon interest rate.

- The money is given to you in a lump sum.

- You are free to utilize the money as you wish or in accordance with any requirements set by the loan terms. For example, in an auto loan, the money is typically paid directly to the dealership, while in a personal loan, the funds are transferred directly to you.

- You repay the loan through regular installments, which can be weekly, biweekly, or monthly, based on a predetermined amount.

- Once you complete the specified term of the loan (the length of time agreed upon to repay it), the contract concludes.

Now, let’s consider credit that is not classified as a loan. Revolving credit serves as a prime example of this distinction, and it includes credit cards and lines of credit. When a company approves you for a credit card, they are extending credit to you, but it does not constitute a loan. Here are some notable differences:

| A Loan | Revolving Credit Such as a Credit Card |

| The entire sum of money is provided upfront. | You have the flexibility to utilize the money from the credit line based on your specific needs. |

| Repayment occurs through fixed installments of a predetermined amount. | The monthly payment requirement is flexible, and determined by the amount of credit you have utilized. It may vary depending on how much of the credit you’ve used. |

| The loan is disbursed once, and you gradually repay it over time. | With a line of credit, you have the convenience of drawing funds repeatedly. As you repay the borrowed amount, you can access the credit again, creating a revolving cycle of borrowing and repayment. |

Differences between Obtaining a Loan and Other Types of Credit

Generally, there isn’t a significant contrast between acquiring a loan and obtaining other types of credit. Both necessitate an application process, and lenders for both options may consider similar factors when evaluating your eligibility.

While some loans may require a specific purpose, like purchasing a vehicle or consolidating debt, many personal loans don’t impose such restrictions. These loans provide the flexibility to borrow funds for any legal purpose without disclosing the intended use.

Likewise, credit options can vary based on their intended use. For instance, a business line of credit differs from a line of credit designed for shopping at a particular retail store. However, with general credit cards or home equity lines of credit, you are not obligated to specify a reason for usage or limit your purchases to certain categories.

Determining which type of credit is easier to qualify for depends on various factors, including the lender’s policies, the amount sought, and your own financial circumstances. Some credit cards and loans are tailored to individuals with good or excellent credit scores, while others are available to those with less impressive credit histories.

Understanding the Distinction Between a Loan and Your Credit History

While a loan is a component of your credit history and can influence your credit score, it is not synonymous with your personal credit or credit history.

When you take out a loan, the lender typically reports the loan to at least one credit bureau. Timely payments on the loan are also reported, just like any missed payments or defaults.

Meeting loan payment obligations can have a positive impact on your credit score, while missed payments or loan defaults can adversely affect it.

Apply for a Loan Today

Whether you urgently require funds and lack access to a line of credit or if you wish to enhance your credit history by responsibly managing a loan, Wise Loan can assist you. We report to credit bureaus and are committed to responsible lending, enabling our customers to make sound financial decisions for their future. Upon approval, you can receive funding on the same day or the next day.

Discover how Wise Loan can aid you and apply for a loan today.

The recommendations contained in this article are designed for informational purposes only. Essential Lending DBA Wise Loan does not guarantee the accuracy of the information provided in this article; is not responsible for any errors, omissions, or misrepresentations; and is not responsible for the consequences of any decisions or actions taken as a result of the information provided above.

More information on Installment Loans and how they work in your state: