When applying for a loan, whether online or in person, it is common for lenders to inquire about the purpose of the funds. While some borrowers may find this intrusive, it is essential to understand that the reason for the loan matters to the lender. They are investing in your request and expect a return on that investment. Moreover, knowing how you plan to use the money allows the lender to assess your suitability as a borrower.

Furthermore, the purpose of the loan can influence the type of loan product that best suits your needs. For instance, if you intend to purchase a car, a vehicle loan often comes with a lower interest rate compared to an unsecured personal loan.

Different lenders have distinct policies, and they may not offer loans for certain purposes. For example, a lender specializing in small installment loans for emergencies may not provide funding for business ventures. It is crucial, therefore, to conduct research before applying for a loan to ensure that the lender’s offerings align with your needs. This way, you can avoid unnecessary denials and potential negative impacts on your credit report due to multiple inquiries.

Regarding personal loans, the usage of funds is usually flexible, depending on the lender’s policies. Some lenders don’t even ask for the purpose of the loan; as long as you meet their requirements, you’re approved, and how you use the money becomes your discretion, as long as you repay it according to the agreement.

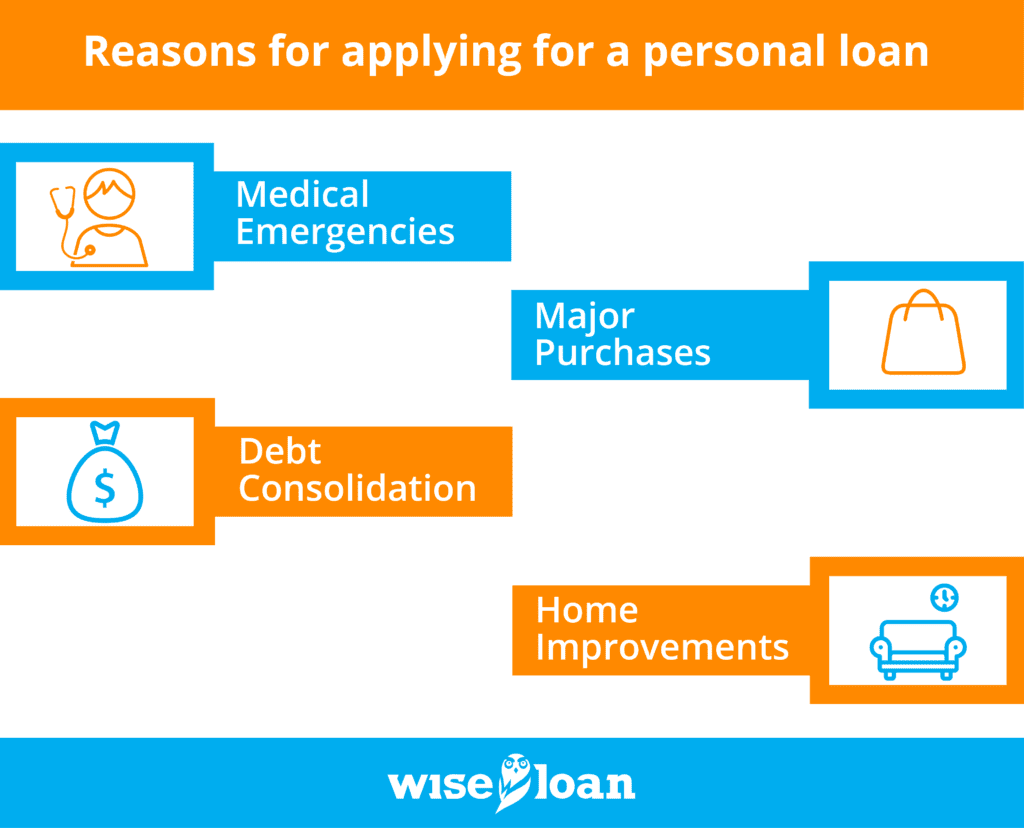

However, it can be helpful to consider common and acceptable reasons for applying for a personal loan. These include:

- Medical Emergencies: Unplanned medical expenses can strain your budget, and a personal loan can be a practical solution to cover these bills and prevent negative consequences on your credit score.

- Debt Consolidation: If you have high-interest debts, such as credit card balances, consolidating them with a personal loan can lead to more manageable payments and potentially faster debt repayment.

- Major Purchases: Personal loans can facilitate significant purchases, like appliances, electronics, or jewelry, especially when you don’t have sufficient savings or wish to preserve your emergency fund.

- Home Improvements: Funding home improvement projects through installment loans can be a viable option, enabling you to enhance your living space.

Personal loan requirements vary among lenders but commonly include a legal address in the applicable jurisdiction, a checking account for depositing funds, proof of income, and a credit score that meets the lender’s minimum criteria. For those with bad credit, certain lenders may still provide personal loan options.

When applying for a personal loan online, it’s advisable to follow these steps:

- Use a personal loan calculator to determine affordable payment options.

- Research reputable and responsible lenders.

- Review available loan options and select the most suitable one.

- Carefully complete the online application, checking for accuracy to avoid unnecessary rejections.

- Be patient during the processing period and refrain from clicking multiple times or closing the window.

- Be available to respond to any follow-up questions or requests for additional information.

In the case of individuals with no credit history, some lenders, like Wise Loan, are willing to consider alternative factors beyond credit scores for loan approval. Applying with such lenders may offer a chance to qualify for a personal loan.

The recommendations contained in this article are designed for informational purposes only. Essential Lending DBA Wise Loan does not guarantee the accuracy of the information provided in this article; is not responsible for any errors, omissions, or misrepresentations; and is not responsible for the consequences of any decisions or actions taken as a result of the information provided above.

More information on Installment Loans and how they work in your state: