Determining whether having a completely clean credit slate is better than having a bad credit score or history when applying for a loan or other forms of debt is a complex matter. It varies depending on several factors involved in money and credit. To gain a better understanding, continue reading below.

What Does No Credit Mean?

Having no credit typically means that you do not have a credit score. A credit score is not generated when there is insufficient recent credit history available for scoring models to calculate a score.

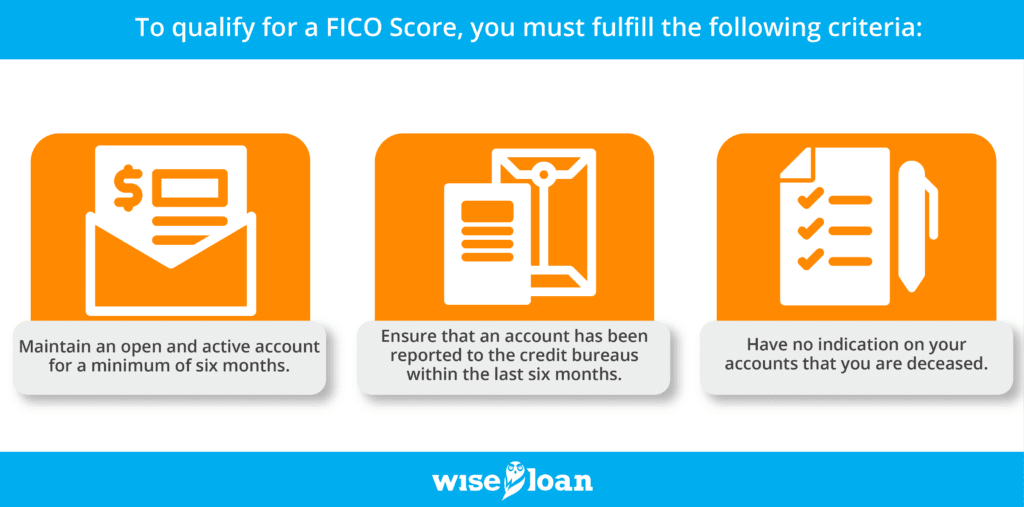

To qualify for a FICO Score, you must fulfill the following criteria:

- Maintain an open and active account for a minimum of six months.

- Ensure that an account has been reported to the credit bureaus within the last six months.

- Have no indication on your accounts that you are deceased.

On the other hand, to obtain a VantageScore 3.0 credit score, you only need one tradeline reported in your credit history, regardless of its age.

It is important to understand that you can have “no credit” with one credit bureau while still having a credit history with others. There are three major credit bureaus, and not all lenders report to all three. If your lender only reports to one credit bureau, your credit score will be generated based on the information contained within that specific bureau’s files.

What Does Bad Credit Mean?

Bad credit typically encompasses both your credit score and the information contained in your credit profile. A good credit score is generally considered to be above 660 or 670, depending on the credit scoring model being used. Scores below this range are categorized as very poor, poor, or fair, and are often referred to as “bad credit” when evaluating creditworthiness for loan or credit card applications.

The main distinction between bad credit and no credit is that bad credit suggests that you have made certain financial mistakes. These mistakes may include missed payments, loan defaults, or managing your accounts in ways that are perceived as irresponsible based on the available records. To gain a better understanding of what can contribute to bad credit, it is important to learn about the factors that can lower your credit score.

What Does Thin Credit Mean?

Having thin credit means that you have a credit history, but it is not substantial enough to generate a good credit score. This situation can occur even if you have consistently made timely payments and managed your accounts responsibly. Credit scores consider various factors, including the age and diversity of your credit, credit utilization, and the number of inquiries on your account. Therefore, it takes time for individuals new to credit to establish a strong credit score. Building up a favorable credit score requires patience and a consistent track record of responsible credit management.

Which Is Worse: No Credit or Bad Credit?

When it comes to obtaining a loan or other opportunities based on your credit score, the question arises: is it better to have no credit or bad credit? The answer depends on the situation, but in many cases, having any credit is preferable.

For instance, when applying for a car loan, lenders typically assess your credit history. If you have no credit history at all, you become an enigma to the lender. They lack the necessary information to evaluate the level of risk involved. As a result, some banks may outright refuse to work with you.

On the other hand, if you have bad credit, the lender has some information to consider. They can observe that you may pose a higher risk as a borrower. However, they may also notice that you have taken steps within the past year to improve your credit, even if the overall score is lower than desired. In such cases, the lender might offer you a loan at a higher interest rate compared to someone with good credit.

In this context, having bad credit becomes a better option if the goal is to secure a vehicle. While you may end up paying more due to the higher interest rate, you still have the opportunity to obtain the loan.

How Can You Start Building Credit If You Don’t Have Any?

If banks are hesitant to work with you due to the absence of a credit score, you may wonder how you can ever establish one. Rest assured, there are numerous products and options available specifically designed to assist individuals in initiating their credit-building journey. The key lies in selecting the right option that aligns with your financial goals and requirements. Here are several options to help you begin building your credit history.

Get a Cosigner

If you find yourself in a situation where you require a loan, such as for a car, and you lack a credit history or possess a poor credit score, you may need the assistance of a cosigner. A cosigner is an individual with a stronger credit profile, perceived by the bank as a lower risk compared to you. When this person cosigns the loan, they effectively agree to assume responsibility for repaying the loan if you fail to fulfill your payment obligations.

Subsequently, the lender reports the loan payments to the credit reports of both you and the cosigner. This enables you to begin establishing a credit history that may alleviate the need for a cosigner in the future.

This option is particularly beneficial if you genuinely require a significant purchase, such as a car, and need to finance it through credit. However, it is essential that you find someone with a satisfactory credit standing who is willing to serve as a co-signer.

Apply for a Secure Credit Card

Not everyone has the opportunity to find someone willing or able to cosign a loan, and not everyone needs to commence their credit-building journey with that level of commitment. An alternative option is to apply for a secured credit card.

A secured credit card functions by requiring a deposit from you, which then serves as collateral for the card. The deposit you make determines your initial credit limit. By using the card responsibly and making timely payments, you may have the chance to increase your credit limit or even have your deposit returned. Moreover, the credit card company typically reports your activity to one or more credit bureaus, enabling you to build your credit history.

This option is particularly suitable if you do not require immediate borrowing but are focused on establishing and strengthening your credit. However, it is important to note that you will need to have approximately $200 or more available to put down as a deposit in order to secure an initial credit line. Applying for a secured credit card can be advantageous if you lack revolving accounts on your credit history. Lenders prefer to see evidence of your ability to manage different types of accounts and the credit mix you have plays a role in determining your credit score.

Get an Installment Loan

If you already have a credit card or find yourself in need of funds for an emergency situation, you can consider building your credit by obtaining an installment loan. Look for lenders like Wise Loan that are more lenient with credit requirements and are willing to assist you in building your credit as you repay the loan.

This option can be particularly beneficial if you want to diversify your credit mix by adding an installment loan to your accounts, or if you require immediate funds for an unexpected expense.

With Wise Loan, you do not need to possess excellent credit to be approved for a loan. Discover more about their offerings and submit your application today to explore the possibilities of improving your credit.

The recommendations contained in this article are designed for informational purposes only. Essential Lending DBA Wise Loan does not guarantee the accuracy of the information provided in this article; is not responsible for any errors, omissions, or misrepresentations; and is not responsible for the consequences of any decisions or actions taken as a result of the information provided above.

More information on Installment Loans and how they work in your state: