Understanding the Credit Check Process: What You Need to Know

The credit check process can be perplexing for many individuals. When applying for a loan or credit card, you might discover that you don’t qualify due to your credit history. To shed light on this process, let’s delve into what a credit check entails and why it is conducted, while also exploring ways to check your credit on your own and potentially get approved for a loan without undergoing a full credit check.

What Is a Credit Check?

A credit check is conducted when someone examines your credit score and/or credit report. This is done for various reasons, such as assessing your creditworthiness as a borrower or evaluating whether you might be a high-risk tenant, employee, or insurance customer.

Hard Inquiry vs. Soft Inquiry:

Credit checks come in two main types: soft and hard inquiries.

Soft inquiries can happen with or without your permission, depending on the entity making the request. These are often used by lenders to pre-evaluate you for a credit offer, such as when you receive a pre-approved credit card offer. Soft inquiries can also occur during employment background checks or when applying for auto insurance or utility services. Importantly, soft inquiries do not impact your credit score, and they are usually only visible to you, not lenders or others checking your credit.

On the other hand, hard inquiries can only occur with your explicit permission and are conducted when you apply for a loan or any other form of credit, as lenders evaluate your application. Unlike soft inquiries, hard inquiries can have a slight negative effect on your credit score for up to a year, and they remain on your credit report for two years. Multiple hard inquiries in a short period may make you appear as a risky borrower, so it’s essential to apply for credit judiciously and when necessary.

How Is a Credit Check Performed?

Most lenders and entities performing hard credit checks use computer software programs to instantly assess your credit. However, they require your permission to do so, which is usually obtained when you apply for credit and provide your signature.

How Are Credit Scores Calculated?

Credit scores are determined using complex scoring models, with FICO and VantageScore being two common ones. Different versions of these models can lead to slight variations in your credit score, depending on which credit bureau is used or which agency pulls the report.

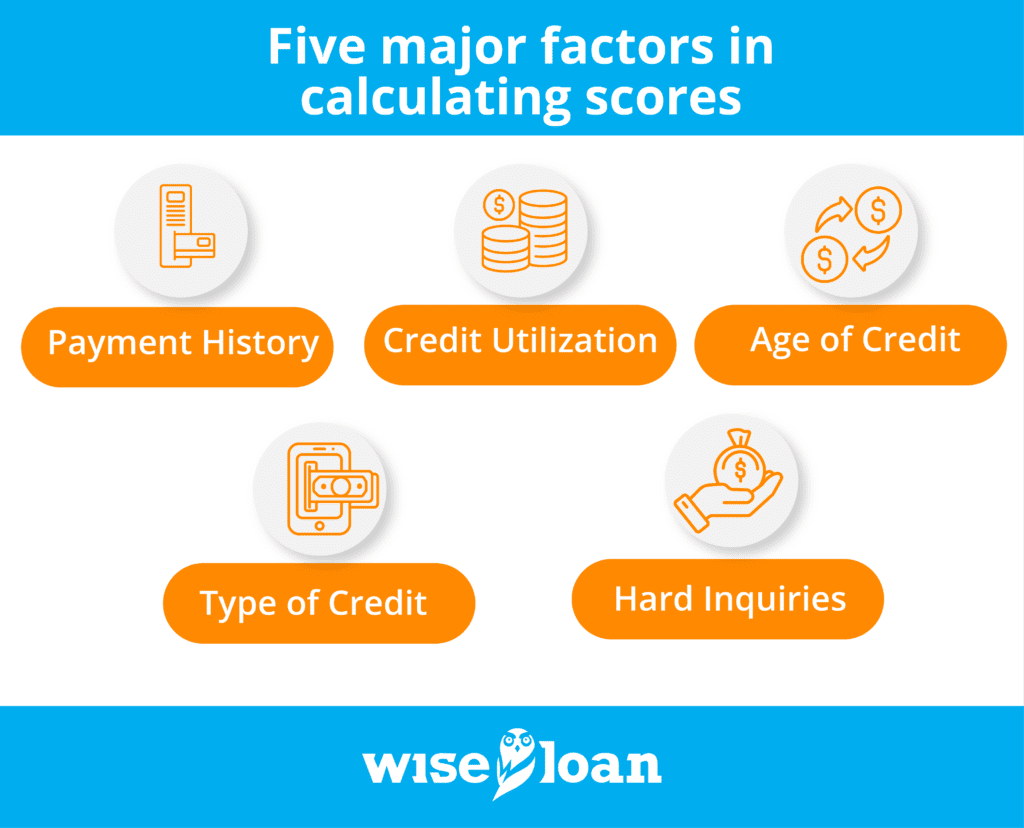

Despite these differences, credit scoring models typically consider five major factors in calculating scores:

- Payment History: The most significant factor affecting your credit score. Timely and consistent payments are crucial, while late payments, delinquent accounts, foreclosures, or collections can negatively impact your score.

- Credit Utilization: The percentage of your available revolving credit that you are currently using. Lower credit utilization rates are generally better for your score.

- Age of Credit: This includes the length of your credit history and the average age of all your open credit accounts. A well-established and positive credit history can improve your score.

- Type of Credit: Creditors and scoring models prefer to see a healthy mix of credit accounts, including both installment and revolving credit, indicating responsible management of various accounts.

- Hard Inquiries: The number of hard inquiries made on your account within the past 12 months can influence your credit score.

Who Can Check My Credit Report?

Several entities have the authority to check your credit report, including lenders, employers, landlords, and certain service providers like insurance and utility companies, provided you give them permission. Some lenders may even access your report with a hard inquiry even if you don’t grant them a soft inquiry.

Concerns about the accessibility of credit report information are common, with worries about identity theft or misuse. To address these concerns, you have the option to temporarily freeze your credit, preventing access for a specific period. To do this, contact the relevant credit bureau and request a credit freeze, which can be undone when needed. Keep in mind that you must separately freeze and unfreeze credit with each of the three major credit bureaus: TransUnion, Experian, and Equifax.

How to Get Your Own Credit Report

You can obtain a copy of your credit report through AnnualCreditReport.com for free once a year from each of the main credit bureaus. Alternatively, various providers offer access to your full credit report more frequently for a fee. If you have been denied credit or services based on your credit report, you have the right to know, and the entity denying you must provide a letter indicating which credit reporting agency provided the data. With this letter, you can request a copy of your report in writing from the agency.

What Is a Good Credit Score?

The definition of a good credit score depends on the scoring model used and the purpose for which you need the credit score. Equifax, for example, considers a credit score of 670 or higher as good or better.

How to Get a Good Credit Score

Building or improving your credit score involves responsible credit use. Keep your credit utilization low and make payments in a timely manner. Ensure that your lenders report your timely payments to credit bureaus. Regularly checking your credit and disputing any inaccurate negative information with credit bureaus can also be beneficial.

How to Bypass a Full Credit Check When Applying for a Loan

If you need immediate funds and are concerned about your less-than-perfect credit history, there may be a way to bypass a full credit check. Consider applying for a personal loan through Wise Loan, which offers an application process taking less than five minutes.

Apply today and explore your options!

The recommendations contained in this article are designed for informational purposes only. Essential Lending DBA Wise Loan does not guarantee the accuracy of the information provided in this article; is not responsible for any errors, omissions, or misrepresentations; and is not responsible for the consequences of any decisions or actions taken as a result of the information provided above.

More information on Installment Loans and how they work in your state: