Soft Inquiry vs Hard Inquiry: Can Applying for a Loan Effect My Credit Score?

Applying for a loan can indeed have an impact on your credit score, regardless of whether you make timely payments and adhere to the agreed terms. It’s important to note that even the act of submitting a loan application can have a slight influence on your credit score. To gain a better understanding of how your credit score can be affected by applying for credit, it’s essential to distinguish between soft inquiries and hard inquiries. This knowledge applies regardless of whether you are approved for the credit you sought.

What Is a Soft Inquiry?

Soft inquiries are instances where your credit score or report is checked by someone, but they do not have an impact on your credit score as per credit scoring models. Interestingly, these inquiries do not appear on your credit report when accessed by others for that purpose; however, you can view them when reviewing your own credit score.

Here are some common situations that typically result in soft inquiries:

– Accessing your own credit report or score, regardless of the reason

– An insurance company assessing your credit score as part of their risk evaluation before offering you a policy

– Your existing creditors reviewing your credit report for routine administrative purposes

– An employer conducting a background check that involves examining your credit

– Credit card companies or other lenders reviewing your score or report to determine your eligibility for a pre-approved credit offer

– Government agencies, like the IRS, utilize information from your credit report to verify your identity during online service registrations.

What Is a Hard Inquiry?

Hard inquiries typically occur when your credit is checked as part of the evaluation process for a loan or other forms of credit. Unlike soft inquiries, hard inquiries are visible on your credit reports and are factored into credit scoring models, potentially impacting your credit score.

Here are several situations that can trigger a hard inquiry:

- Credit applications result in lenders accessing your credit report, including auto loans, private student loans, personal loans, mortgages, and credit cards.

- Requests for credit limit increases, prompting your current creditor to review your credit report when considering extending more credit.

- Applications for renting a residence or establishing new utility services.

- In some instances, when collection agencies perform skip tracing to locate individuals, it can be recorded as a hard inquiry on your credit report.

Do Hard Inquiries Lower Your Credit Score?

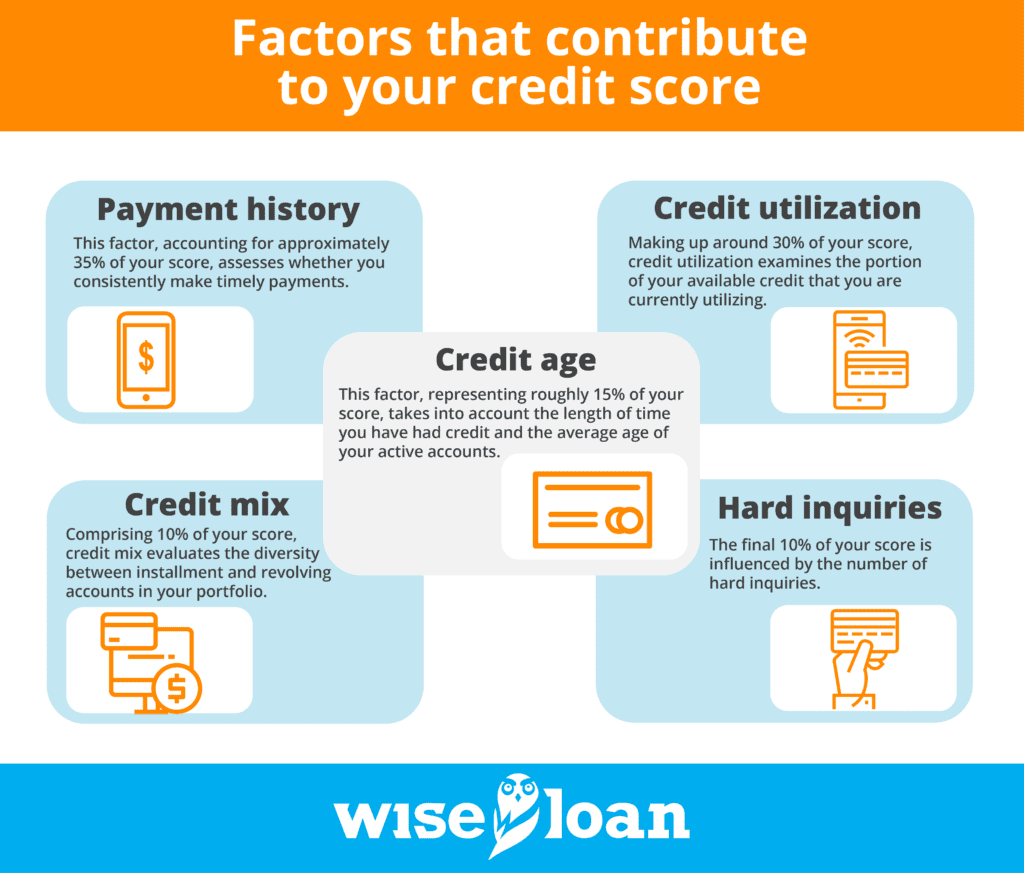

Indeed, hard inquiries have the potential to temporarily decrease your credit score. It’s essential to consider the various factors that contribute to your credit score and understand their approximate significance within credit scoring algorithms:

While hard inquiries are not the primary factor affecting your score, they do hold significance. Each new inquiry can lead to a small decrease in your score, and multiple inquiries can accumulate, resulting in a more substantial impact.

Furthermore, lenders may view numerous inquiries within a short timeframe as a red flag. This pattern may suggest financial instability or a desperate need for additional credit, which can raise concerns about an individual’s ability to fulfill new debt obligations as agreed.

The Exception of Rate Shopping

Rate shopping involves applying with multiple lenders to secure the best interest rate when seeking an auto loan, mortgage, or student loan. Engaging in rate shopping does not indicate poor financial health. On the contrary, it demonstrates prudent financial habits and knowledge as you strive to make the most informed financial decisions. Consequently, when it comes to these specific loan types, credit checks conducted within a brief period are typically treated as a single hard inquiry by scoring models.

FICO scoring models generally allow for a 45-day rate shopping period, enabling you to explore rates for over a month without detrimental effects on your credit score. However, VantageScore scoring models have a shorter window of 14 days, meaning it is advisable to complete your applications within a two-week timeframe whenever feasible.

It’s important to note that these rate shopping periods do not apply to credit card applications and may not be universally applicable to all types of loans. While car and mortgage loans commonly fall within these guidelines, it is prudent to consult your lender or broker when applying for other types of credit to understand how multiple applications may impact your credit.

What Type of Inquiry Do Lenders Use to Check Credit Health?

When assessing individuals for loans or credit cards, lenders commonly employ hard inquiries to gather information about their credit history. However, it’s worth noting that not all lenders follow this practice, as certain institutions provide loans or credit cards that do not necessitate a credit check.

It is crucial to recognize that even if a loan or credit card is advertised as not requiring good credit, it does not necessarily mean that the application will be exempt from a credit check. Lenders may still examine your credit report to gain a comprehensive understanding of your financial background before extending credit or offering a personal loan. To ensure clarity, it is advisable to carefully review the terms and conditions of any application to ascertain the specific requirements involved.

Wise Loan installment loans are an example of credit services that do not mandate excellent credit. To gain a deeper understanding of how Wise Loan‘s offerings function, further information can be obtained regarding their services.

How Many Credit Inquiries Are Too Many?

It is highly advisable to minimize the number of hard inquiries whenever possible. This entails refraining from applying for credit impulsively or when there is a high likelihood of rejection. Instead, it is recommended to conduct thorough research on available credit opportunities and apply for loans or credit options that align with your needs and have a higher likelihood of approval.

There is no specific threshold for determining how many hard inquiries are excessive. The impact of inquiries on your credit score and credit eligibility varies based on your overall credit health, as well as other factors such as income and debt utilization. However, FICO acknowledges that individuals with five or more inquiries within the past year are more prone to late payments, while those with even greater numbers of inquiries within a short timeframe are significantly more likely to face bankruptcy compared to those with no inquiries.

How Long Do Inquiries Stay on Your Credit Report?

Both hard and soft inquiries can remain on your credit report for a maximum of two years, although some inquiries may only be visible for one year. However, it’s important to note that the impact of hard inquiries on your credit score lasts for only one year, and their influence gradually diminishes over time.

This is indeed reassuring news. If you have mistakenly applied for multiple forms of credit within a condensed timeframe before coming across this article, rest assured that your credit has not been permanently damaged, nor has your score been irreversibly reduced. By adopting a more responsible approach to future loan and credit applications, the impact of those hard inquiries will gradually diminish and eventually disappear over time.

How Long Should You Wait to Apply for a Loan After a Hard Inquiry?

How long should you wait between credit report inquiries to minimize their impact? The answer depends on your financial objectives and requirements. If you have plans to apply for a significant loan, such as a mortgage or car loan, in the near future, it is advisable to avoid additional hard inquiries altogether. Additionally, it is crucial to avoid accumulating more debt during this period, as an increased debt-to-income ratio could jeopardize your approval for a mortgage or car loan.

What if you recently received a loan or just applied for one? Can you immediately pursue another form of credit, such as a credit card? While some individuals may be eager to diversify their credit mix with good intentions, it’s important to remember that building credit is a long-term endeavor rather than a hasty race. If your primary goal is to improve your credit score, it might be wise to take your time and space out your credit and loan applications. This approach allows for a more measured and strategic approach to managing your credit and achieving your desired credit score enhancement.

Improve Your Credit Score With Wise Loan

At Wise Loan, we understand that having excellent credit is not a requirement for loan approval. In fact, we provide a range of services and features specifically designed to assist you in enhancing your credit through our personal loans. By consistently and responsibly managing your loan, including making timely payments, you have the opportunity to improve your credit score. It is worth noting that Wise Loan reports your loan activity to two out of the three major credit bureaus. This is particularly valuable since it ensures that your credit information is available to potential lenders regardless of which credit service they utilize to access your report.

Find out more about Wise Loan loans and apply for yours today.

The recommendations contained in this article are designed for informational purposes only. Wise Loan does not guarantee the accuracy of the information provided in this article; is not responsible for any errors, omissions, or misrepresentations; and is not responsible for the consequences of any decisions or actions taken as a result of the information provided above.