In recent times, tax refund anticipation loans have become increasingly prevalent.

Essentially, borrowers can engage a tax professional to estimate their expected refund amount. For a fee, they can receive a cash advance, granting them early access to their refund and ensuring timely completion of their upcoming tax filing.

This arrangement typically benefits all parties involved. The tax professional or company gains a head start on tax-season business, building a loyal customer base in the process.

However, for one family in New Mexico, their holiday plans in 2016 took an unfortunate turn due to a refund anticipation loan. The DeJolie family received such a loan in November 2017, which allowed them to cover holiday expenses. Now, they’re taking legal action against the tax service company that issued the loan. The lawsuit alleges that the company failed to accurately disclose the annual percentage rate (APR) and additional charges for the tax preparation services in the loan documentation. The DeJolie family contends that while the stated APR was 264%, hidden charges and fees buried in the fine print inflated the “true” APR to a staggering 385%.

Adding to their grievances, the DeJolie family asserts that they were billed $157.05 for the tax preparation portion of the loan, yet the invoice they received during signing only showed $145. Additionally, a $9.75 charge for a credit check was levied.

While this lawsuit remains unresolved, it highlights a situation that many individuals might encounter as these loan types gain popularity.

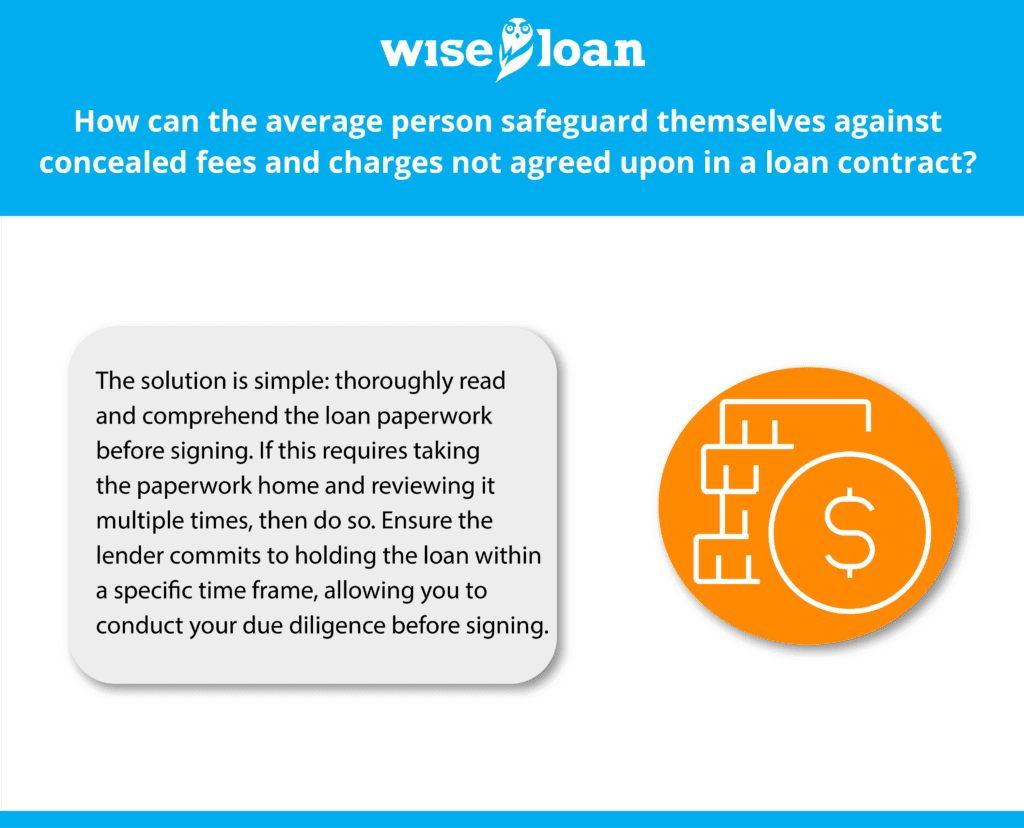

How can the average person safeguard themselves against concealed fees and charges not agreed upon in a loan contract?

The solution is simple: thoroughly read and comprehend the loan paperwork before signing.

To emphasize:

Read the loan documents carefully and ensure full understanding before putting pen to paper and signing!

If this requires taking the paperwork home and reviewing it multiple times, then do so. Ensure the lender commits to holding the loan within a specific time frame, allowing you to conduct your due diligence before signing. By doing this, you protect your rights and gain detailed knowledge of the commitment you’re entering.

There’s no excuse for neglecting the fine print.

A lender cannot legally compel you to sign a loan contract, and you must be aware of your rights before succumbing to pressure for a loan you can’t afford. If a lender refuses to allow you time for independent review of the paperwork or insists on immediate signing, consider taking your business elsewhere. If they were transparent in the paperwork, there’d be no need to rush you.

That’s correct—there’s no reason for undue haste.

Don’t allow them to diminish the importance of your rights. Take your time, or be prepared to face the consequences. It’s your money and peace of mind; both must be protected.

The recommendations contained in this article are designed for informational purposes only. Essential Lending DBA Wise Loan does not guarantee the accuracy of the information provided in this article; is not responsible for any errors, omissions, or misrepresentations; and is not responsible for the consequences of any decisions or actions taken as a result of the information provided above.