Get ready for Tax Season! It feels like just a week or two ago when we were celebrating Christmas dinner with our loved ones. But now, it’s time to tackle the numbers again, and we eagerly await the day our refund check arrives.

However, waiting is no longer necessary because you have the option of getting a refund anticipation loan (RAL). These loans are offered by lenders who promise to deliver the money from your tax return to you immediately, without any delay.

Before you get too excited, remember the saying “If it sounds too good to be true, it probably is.” Momma was right about that.

It’s essential to understand that RALs are not offered by legitimate tax preparation companies; those are known as Refund Advances, backed by trustworthy tax preparation firms. RALs, on the other hand, come from other sources and often have harsher terms, making them not worth it in the end.

How Refund Anticipation Loans Work:

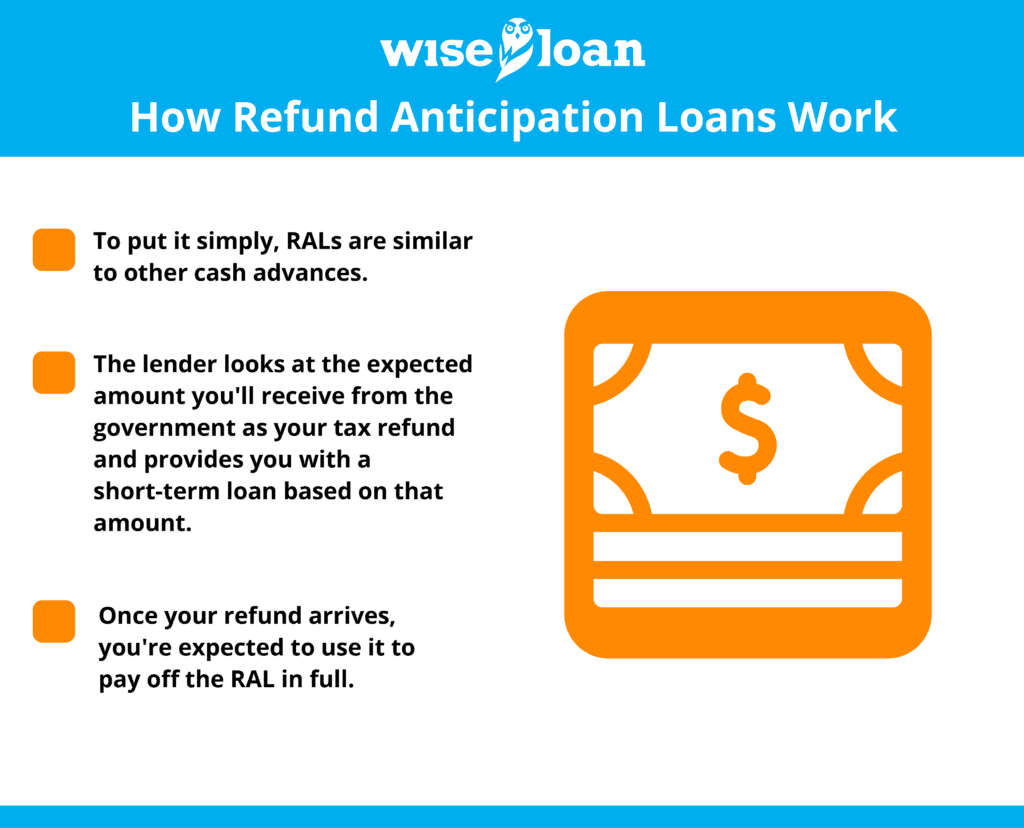

To put it simply, RALs are similar to other cash advances. The lender looks at the expected amount you’ll receive from the government as your tax refund and provides you with a short-term loan based on that amount. Once your refund arrives, you’re expected to use it to pay off the RAL in full.

However, some lenders impose exorbitant interest rates on RALs, sometimes reaching the levels of payday loans. In the past, a couple from New Mexico took out a $1,250 RAL and ended up being charged almost 400% interest. They aren’t the only ones facing this issue, as many families have struggled with RALs and some are fighting legally against these predatory practices.

Moreover, some lenders add extra fees on top of the interest, reducing the loan amount significantly. For example, if you were expecting a $5,000 refund, you might only be offered a short-term loan of $1,500 with an additional $1,700 in fees.

Are any RALs safe?

You might already know that choosing a storefront or popup lender is a bad idea for an RAL. But what about the reputable tax preparation companies like H&R Block and Jackson Hewitt? They do offer RALs to clients with no fees or interest, but it’s crucial to understand the fine print.

While they advertise “fee-free” or “zero percent APR,” there’s still a cost. To qualify for an RAL, you have to pay the company to prepare your taxes, which could amount to several hundred dollars depending on the complexity of your returns. This amount is deducted from your refund on the back end, so if you filed your taxes independently, you’d likely receive a larger refund.

Additionally, there’s a risk that the RAL amount won’t match your actual refund. If you take an RAL for $3,000, but your actual refund is only $2,000 due to deductions like unpaid child support or traffic tickets, you’ll still be responsible for repaying the full loan.

Instead of going for an RAL:

Consider filing your taxes on your own as soon as possible. Credit Karma offers free tax preparation and e-filing, which eliminates the need for extra paperwork or trips to the post office. By choosing direct deposit, you could receive your refund within 10 to 21 days, much faster than waiting for a month.

If you still require a short-term loan, consider Wise Loan as a reliable option. Give us a call today for assistance.

The recommendations contained in this article are designed for informational purposes only. Essential Lending DBA Wise Loan does not guarantee the accuracy of the information provided in this article; is not responsible for any errors, omissions, or misrepresentations; and is not responsible for the consequences of any decisions or actions taken as a result of the information provided above.