As the year comes to a close, it’s essential to assess your family’s contingency plan in case of a crisis. Have you ever thought about what would happen if unexpected hefty expenses arise? What if you couldn’t explain the funding sources and assets available to tackle the crisis?

Many people neglect having a contingency plan in place, but addressing this is crucial before a crisis strikes. Informing your family about your wishes and financial strategies during a crisis ensures that you won’t be bombarded with questions about various accounts and assets when the crisis hits. This way, your family can offer support when you need it the most, allowing you to focus on overcoming difficult times.

Some families worry about maintaining financial confidentiality, especially when family dynamics are complex. Disclosing account balances and asset specifics might deter adult children from striving for financial independence or stress them when contemplating contributing to their aging parents’ expenses. There are numerous reasons to keep financial information private, depending on individual family situations.

However, silence comes at a cost, particularly during a crisis. When you or your spouse are under stress, trying to educate your family about your financial situation and assets becomes nearly impossible and highly stressful.

To reduce stress and difficulties during a crisis, having a written contingency plan and financial statement of resources is the best solution. Both spouses and a designated “lead child” should know where financial and estate planning documents are kept and have authorized access to them if they are secured. These documents should contain essential information tailored to your circumstances.

Types of income:

By clearly listing the types of income and the earners, the person handling your finances during the crisis will know what to expect. They’ll understand which incomes will continue during the emergency and which may decrease or stop. This includes pensions, Social Security, wages, or salaries if you or your spouse are still employed.

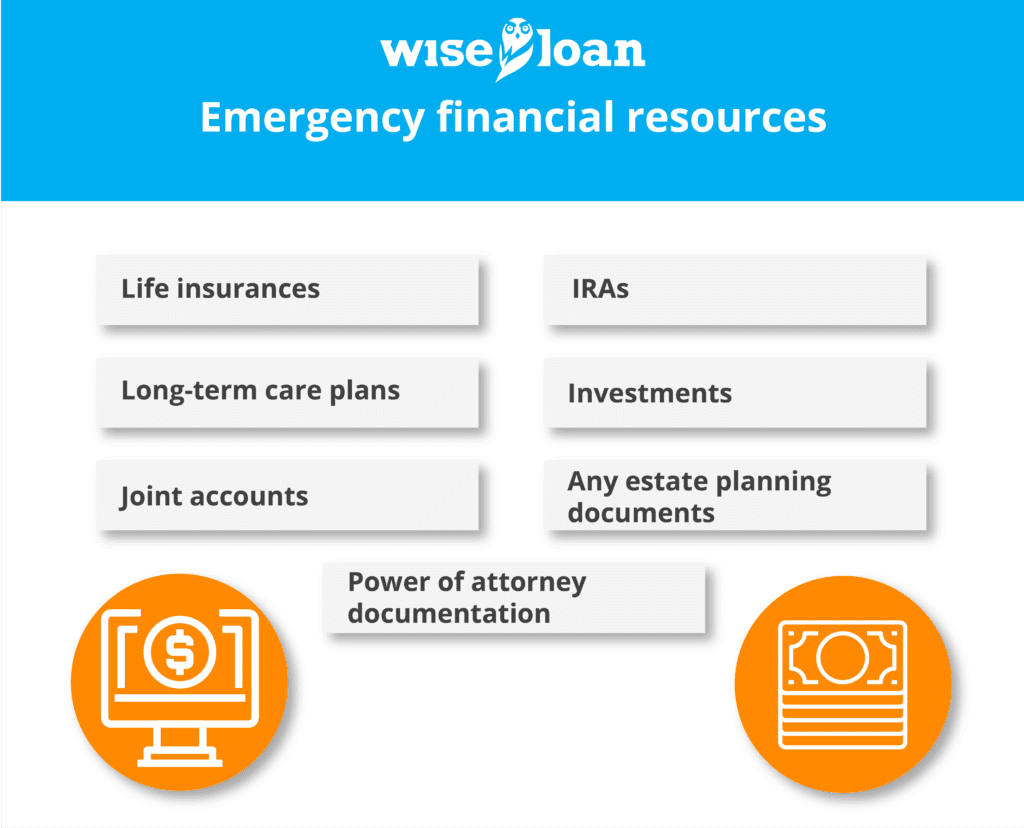

Emergency financial resources:

This list should cover life insurances, long-term care plans, joint accounts, power of attorney documentation, IRAs, investments, and any estate planning documents like a will. Mention how to access each resource, who has access, and its intended use during a crisis. For instance, if your life insurance policy should only be used in case of death, clarify this in your contingency plan. If accessing joint accounts should follow a specific order for maximizing benefits or reducing repayment costs after the crisis, explain the rationale in your documentation.

Your contingency plan aims to provide clarity and ensure your wishes are followed during a crisis when you might not be able to explain things clearly. Be concise and clear, and once it’s in place, take a deep breath and enjoy the new year!

The recommendations contained in this article are designed for informational purposes only. Essential Lending DBA Wise Loan does not guarantee the accuracy of the information provided in this article; is not responsible for any errors, omissions, or misrepresentations; and is not responsible for the consequences of any decisions or actions taken as a result of the information provided above.