With over 21 million personal loans outstanding in the United States, personal loans have become a common form of debt. Many individuals apply for personal loans for various reasons, including debt consolidation, home improvements, unexpected expenses, medical bills, and relocation.

However, it’s important to note that loan approval is not guaranteed, and certain obstacles like a low credit score or a high debt-to-income ratio can hinder your chances. Discover effective strategies to enhance your likelihood of loan approval by reading below.

In this article, we will cover the following topics:

- What is the most accessible loan to get approved for?

- Understanding the four Cs of loan approval.

- How to ensure the approval of your loan application.

- Frequently asked questions about loan approval.

What Is the Easiest Loan to Get Approved For?

If you’re looking to increase your chances of loan approval, one effective strategy is to apply for a loan that offers easy approval. Lenders such as Wise Loan specialize in providing loans that do not require a strong credit history, allowing individuals to access the funds they need while also working towards building credit for the future.

The easiest loan to get approved for is the one that aligns with your qualifications. Prior to initiating the loan application process, it is crucial to have a solid understanding of the four Cs of loan approval: capacity, capital, collateral, and credit. Familiarizing yourself with these factors will help you determine which loan options you are eligible for. At Wise Loan, for instance, we require applicants to have a checking account with direct deposit as part of our qualification criteria.

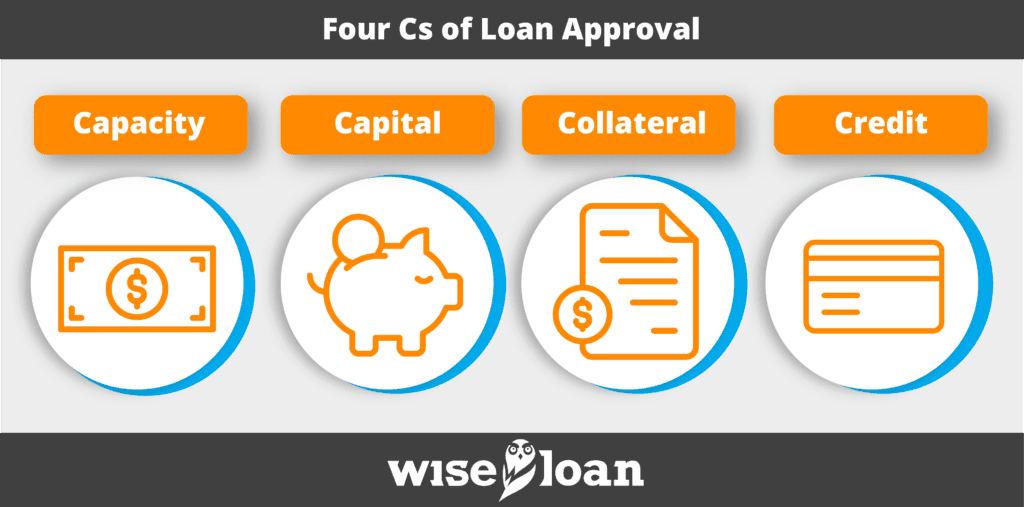

What Are the Four Cs of Loan Approval?

When assessing loan applications, lenders typically consider the four Cs, which are crucial factors in determining loan approval. These four Cs are:

- Capacity: Lenders evaluate your capacity to repay the loan by assessing your income. Most loan applications require documentation to verify your income. If your income is insufficient, it can lead to a loan denial.

- Capital: Some lenders consider the amount of cash you have available. If you have a savings account or emergency fund to cover unexpected expenses, it demonstrates your ability to meet loan payments, even during financial challenges.

- Collateral: Collateral refers to an asset you provide as security for the loan. Secured loans are often easier to obtain because the lender can seize the collateral and sell it to recover losses if you fail to repay. For example, an auto loan is secured by the vehicle, which can be repossessed if payments are not made.

- Credit: Lenders typically review your credit history to assess your track record in managing debt and making timely payments. A good credit history enhances your chances of loan approval.

While all four Cs are significant factors, their importance may vary depending on the loan type. For larger loans, such as mortgages, each factor carries significant weight. However, for smaller personal loans, lenders may have their own policies and might not scrutinize all four Cs as closely.

5 Steps to Make Sure Your Loan Is Approved

To increase your chances of loan approval, take proactive steps to emphasize the four Cs and other crucial factors before applying. Follow the tips below for a better chance of success:

- Apply for the right loan.

Avoid applying for loans that you know are beyond your qualifications. Each time a lender conducts a credit check for a loan application, it results in a hard inquiry on your credit report. Accumulating too many hard inquiries can lower your credit score and give the impression that you are financially desperate, which is not favorable when seeking loans. Instead, conduct thorough research on loan options, understand the required credit and income criteria, and only apply for loans with affordable payments within your means.

- Maintain a healthy debt-to-income ratio

A critical factor in loan approval, including mortgages and personal loans, is your debt-to-income ratio (DTI). This ratio compares your monthly debt payments to your monthly income. A high DTI can lead to loan rejections. For instance, if your monthly income is $3,000 and your monthly debts amount to $2,200, leaving only $800 for living expenses and other bills, lenders are unlikely to approve your loan application because you lack sufficient income to handle additional debt. Therefore, ensure your DTI remains at a reasonable level by managing your debts effectively.

- Improve your credit:

Credit scores often play a significant role in loan approvals. Take steps to enhance your credit score by:

– Making timely payments on all existing accounts.

– Paying down debts, especially on revolving accounts such as credit cards.

– Regularly reviewing your credit reports for potential errors and promptly disputing any inaccuracies.

- Submit all required documentation:

Ensure you carefully follow the application instructions and provide all necessary information and documentation as requested. Failure to provide the required documents may result in a loan denial or unnecessary delays in the approval process. Even for straightforward personal loans like those offered by Wise Loan, you may need to provide proof of identification, a valid address, and a checking account in your name to facilitate electronic deposits for loan funding.

- Stay accessible and responsive:

After submitting your loan application, remain attentive to your email and text messages. Lenders may reach out to seek clarification on certain details or request additional documentation to proceed with the loan approval process. Promptly respond to their inquiries to ensure a smooth and efficient loan evaluation.

If you’re seeking a loan that offers easy qualification and the opportunity to build credit for the future, consider starting with Wise Loan. Apply today, and if approved, you could receive your funds within minutes.

Frequently Asked Questions (FAQs) about Loan Approval

Can a loan that has been approved be denied?

There are situations where a loan that you believed to be approved can be denied. This commonly occurs in mortgage scenarios, where you may have received preapproval for a mortgage loan. However, during the full underwriting process, the lender may decide not to proceed with the loan due to changes in your credit, debt, or income that took place between preapproval and final closing.

In rare cases, an approved auto loan may be denied. This typically happens when there are changes in the loan details or when the lender is unable to verify certain information provided during the application.

Once you have been approved for a personal loan and the funds have been disbursed (received by you), it is generally unlikely for the loan to be denied afterward.

How can I borrow money instantly?

Wise Loan offers an instant funding option for its online loans. To qualify for instant funding, you need to apply and get approved before 5:30 pm CT and have a checking account with a Visa or Mastercard debit card associated with it. With instant funding, you can receive the loan funds on the same day of approval. However, the actual speed of fund transfer depends on your financial institution’s processes. If approved, the money can be deposited into your bank account within minutes. Having a Visa or Mastercard debit card linked to your account is necessary as the instant funds are transferred through the card networks.

Who has the final say in loan approval?

The decision to approve a loan rests with the lenders. In some cases, initial evaluations may be handled by automated systems that use programmed requirements to determine loan eligibility. For instance, if a lender has a minimum credit score requirement of 600, computer systems may automatically reject applicants with scores lower than that.

However, in most cases, a human evaluator also reviews your application. This person could be an underwriter or a trained staff member responsible for assessing your documentation against the lender’s loan criteria.

The recommendations contained in this article are designed for informational purposes only. Essential Lending DBA Wise Loan does not guarantee the accuracy of the information provided in this article; is not responsible for any errors, omissions, or misrepresentations; and is not responsible for the consequences of any decisions or actions taken as a result of the information provided above.

More information on Installment Loans and how they work in your state: