Understanding Good Debt: Building Your Financial Future

When it comes to debt, many people have a knee-jerk reaction to avoid it completely. However, it’s essential to recognize that not all debt is inherently bad. There is a concept called “good debt” that can actually be beneficial for your financial growth and opportunities. Lenders take this into consideration when evaluating loan applications or credit card requests.

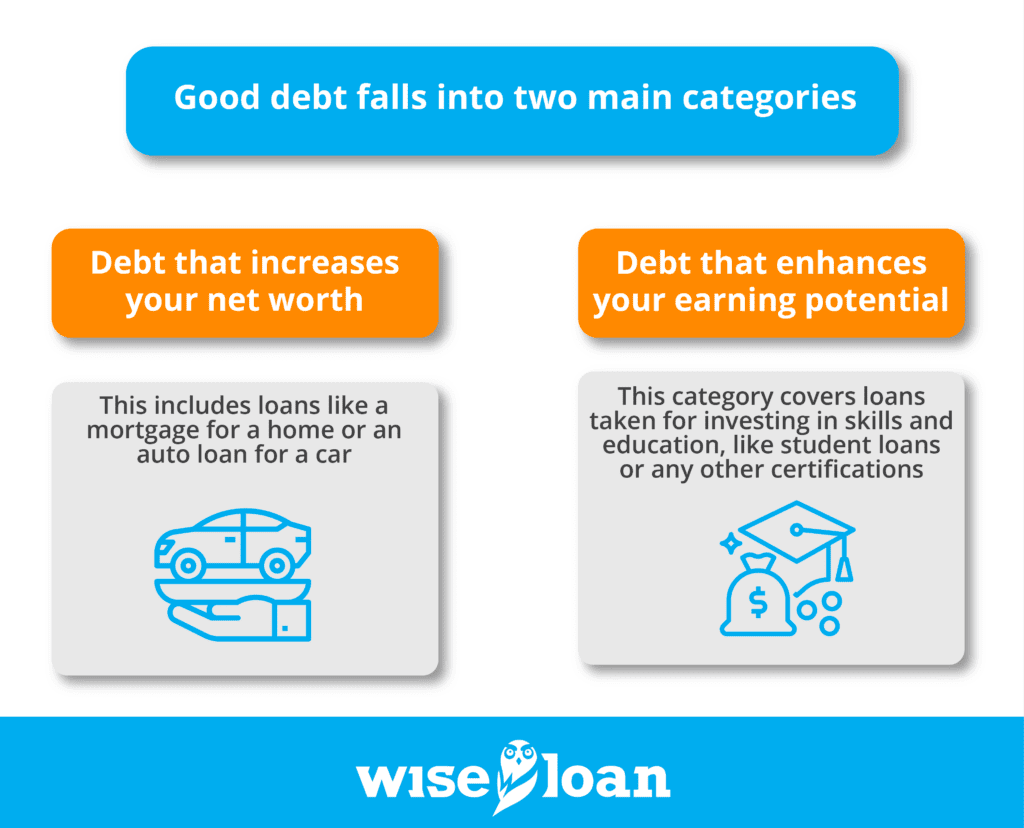

Good debt falls into two main categories:

- Debt that increases your net worth: This includes loans like a mortgage for a home or an auto loan for a car. Although these loans may create a substantial debt initially, they contribute towards owning an expensive asset with real value, such as a property or a new vehicle. Lenders generally view this type of debt more favorably than debt incurred for purely consumptive purposes.

- Debt that enhances your earning potential: This category covers loans taken for investing in skills and education, like student loans or any other certifications that can improve your value in the job market. While some loans may have lower interest rates, any form of education or skill enhancement is considered good debt and can positively impact your creditworthiness.

Another type of good debt is a business loan, which can be used to invest in the growth and future success of a business. Whether it’s expanding your existing business or starting a new venture, this debt is seen as an investment in your financial future by lenders and creditors.

In contrast, bad debt arises from discretionary expenses, such as vacations, luxury purchases, or extravagant dining habits. This kind of debt does not contribute to building assets or increasing earning potential and is generally frowned upon by lenders.

Exceptions to Good Debt:

There are instances where asset-driven or forward-looking debts may not be as advantageous as initially thought. For example, buying an expensive car could lead to a situation where the car’s value depreciates faster than the debt is paid off, leaving you owing more than the car’s worth after selling it.

Medical debt is another gray area. While it may not be elective, significant medical debt can have long-term financial consequences. However, the lack of interest in medical debt can be a silver lining, allowing every dollar spent to directly reduce the debt owed.

Considering a Debt-Free Life:

Living entirely debt-free may seem impractical in today’s world. For essential goals like education, homeownership, or buying a car, taking on some debt is often necessary. The good news is that lenders understand these essential debts and won’t hold them against you when applying for future loans or credit cards. In fact, responsible management of good debt can lead to lower interest rates and more favorable loan terms.

Building Credit History:

Having some good debt can be beneficial for establishing a credit history. In various aspects of life, such as job applications or renting an apartment, a credit check is often required. By managing good debt wisely and minimizing bad debt, you can significantly improve your financial situation, which may not be possible with no debt at all.

The Risk of Good Debt Turning Bad:

It’s crucial to recognize that even good debt can turn into bad debt if not managed properly. Unexpected circumstances like job loss or fluctuating interest rates can turn a home mortgage or educational loan into a financial burden. Therefore, it’s essential to be vigilant and ensure that your debts remain manageable and contribute positively to your overall financial well-being.

Seeking Financial Assistance with Wise Loan:

If you find it challenging to secure a loan for your needs, Wise Loan can provide assistance. Contact us today to check if you qualify for a quick, same-day, or next-day loan. Our application process takes just five minutes, and we provide swift decisions. With easy approval and no hidden fees, you can take control of your financial situation responsibly. Improve your financial future with Wise Loan.

The recommendations contained in this article are designed for informational purposes only. Essential Lending DBA Wise Loan does not guarantee the accuracy of the information provided in this article; is not responsible for any errors, omissions, or misrepresentations; and is not responsible for the consequences of any decisions or actions taken as a result of the information provided above.