It’s the Monday following payday, and you find yourself in a challenging situation. Despite using a significant portion of your Friday’s wages to handle bills and purchase groceries, your car has unexpectedly broken down, leaving you stranded on the roadside. The repairs required to fix your vehicle are uncertain, and you’re concerned about how you’ll manage to cover the costs. Complicating matters further, your car is essential for commuting to work and earning your upcoming paycheck.

Given these circumstances, you may be contemplating whether a payday loan is a viable solution for you. To make an informed decision regarding your immediate financial needs, it’s important to understand how payday loans operate and explore potential alternatives. Delve into the details below and equip yourself with valuable information, ensuring you can navigate through your current emergency with confidence.

What Is a Payday Loan?

A payday loan is a short-term borrowing option designed to be repaid within the next one or two pay periods. It is not intended to offer a long-term solution for financial difficulties, but rather to address immediate cash flow problems that often arise during emergencies or urgent situations.

People may consider payday loans for various reasons, including:

- Managing unforeseen and urgent expenses: When faced with unexpected situations such as an uninsured medical visit, repairing a malfunctioning home air conditioning system, or replacing a broken work tool, individuals may opt for a payday loan to cover these pressing costs.

- Meeting essential needs temporarily: In cases where an unforeseen expense or other unforeseen circumstances have left a family without sufficient funds to purchase groceries or meet other necessary expenses, a payday loan can serve as a temporary means to make ends meet for a week or two.

- Seizing time-limited opportunities: There are instances where individuals may need to finance a time-sensitive purchase, such as an item available at a discounted price for a limited duration, which prompts them to consider a payday loan to cover the cost of the purchase.

It’s important to approach payday loans with caution, considering the associated fees and interest rates. Exploring alternative options and evaluating the potential impact on your overall financial well-being is crucial before making a decision.

How Do Payday Loans Work?

However, is it wise to consider payday loans as a solution, even in urgent situations? To make an informed decision, it’s crucial to have a clear understanding of how payday loans operate. Let’s walk through the step-by-step process of the most common version of a traditional payday loan.

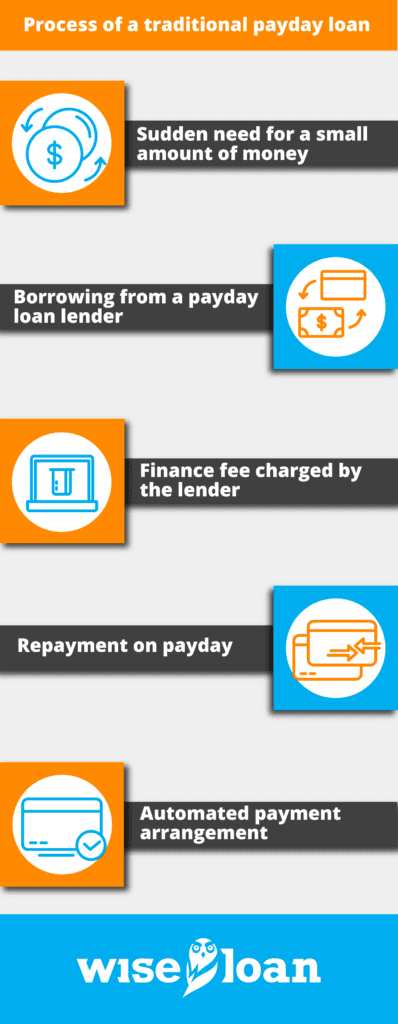

- A sudden need for a small amount of money: Payday loans are designed for quick access to relatively small sums of money, with the expectation that the loan will be repaid with your next paycheck (or the subsequent two paychecks). Keep in mind that as you still have ongoing living expenses like rent, gas, and groceries, the amount you can realistically borrow through a payday loan is limited.

- Borrowing from a payday loan lender: You approach a payday loan lender who agrees to lend you the required amount for a short period, typically no longer than a month.

- Finance fee charged by the lender: The lender levies a finance fee for providing the loan. On average, these fees amount to $15 per $100 borrowed. For instance, if you borrow $500, you would need to pay $75 in finance fees.

- Repayment on payday: The borrowed amount, along with the finance fees, is due to be repaid on your next payday. In the example mentioned earlier, your next paycheck would be reduced by $575 ($288 if the loan is repaid over two paydays).

- Automated payment arrangement: In most cases, payday loan lenders require borrowers to set up automated payments from their checking accounts, ensuring that the agreed-upon amount is automatically deducted. This is also the case with Wise Loan, where automated payments are a part of the payday loan process.

Remember to carefully consider the implications of payday loans, including the associated fees and interest rates. Exploring alternatives and assessing the potential impact on your financial situation is crucial before proceeding with a payday loan.

What Is the Interest on Payday Loans?

You may have observed that the term “interest rate” was not mentioned in the previous explanation of how payday loans operate. This omission stems from the fact that payday loans differ from installment loans, where money is repaid over several months at a predetermined interest rate.

However, this does not imply that payday loans come without costs. The finance fees associated with payday loans can accumulate significantly. When combined with the necessity of repaying the loan within a short pay cycle or two, it can severely restrict your available cash flow, creating a challenging financial situation.

What Is the Payday Loan Trap?

You may have come across the misconception that payday loans are intentionally designed to be impossible to repay, trapping borrowers in a never-ending cycle of finance fees. While this belief is not entirely accurate, it does not mean that the payday loan trap is non-existent.

Here’s how the payday loan trap can unfold in reality:

- Initial loan repayment feasibility: Initially, you take out a payday loan that, on paper, appears to be manageable for repayment. The lender is supposed to ensure that you have the means to repay the loan and provide reasonable repayment options.

- Unexpected financial challenges: However, unexpected circumstances arise. Your grocery bill exceeds expectations, your vehicle requires an expensive tire replacement, or your child’s illness necessitates urgent medical care and medication. As a result, your upcoming paycheck needs to stretch further than anticipated.

- Rolling over the loan: In this situation, you choose to roll over the payday loan into a new loan. This means borrowing the necessary amount to repay the existing loan, including the finance fee. Additionally, a new finance fee is charged. For example, if you initially borrowed $500 with a $75 fee, you now need to borrow $575. If the lender imposes a rollover fee of $50, your total owed amount becomes $625.

- Repeat scenarios: It is possible that a subsequent chain of events may prevent you from repaying the loan once again, leading to rolling over the $625 into a new loan, now amounting to $675. Legitimate payday lenders often have measures in place to restrict this cycle of borrowing, but it still results in a significant finance fee for a very short-term loan.

It’s important to be aware of the potential risks associated with payday loans, including the possibility of falling into a cycle of debt. Exploring alternative options and seeking financial advice can help you navigate challenging situations without resorting to payday loans.

Why Consider a Personal Loan Instead of a Payday Loan?

If you’re in need of fast cash but want to avoid getting trapped in a payday loan cycle, a viable alternative to explore is applying for a fast personal loan online.

Wise Loan offers personal installment loans that can be conveniently applied for in just a few minutes. Qualifying for the loan is possible even with less-than-perfect credit, and we provide instant funding options. Depending on the time of day you complete the application, you may receive same-day or next-day funding. Instant funding is available for those who apply and are approved before 5:30 pm CT, and have a Visa or Mastercard debit card linked to their checking account. The exact timing of receiving funds depends on the processes of your financial institution.

While many of these benefits align with those offered by payday loans, choosing an installment loan from Wise Loan presents potential advantages that most payday lenders cannot provide:

- Flexible repayment terms: Our installment loans offer repayment options spanning a few months or even up to a year or two, depending on the specific loan. This allows for more manageable payments compared to traditional payday loans. For example, in Louisiana, a $700 loan for 5 months might result in bi-weekly payments of $131, enabling you to spread out the payments into affordable amounts and retain more of each paycheck. At Wise Loan, the loan terms are six months for all states, and residents of every state except Texas have the option to request an extended repayment period.

- Credit-building opportunity: Timely payments on our personal loans are reported to credit bureaus, which can contribute to building your credit history. This is a feature typically absent in traditional payday loan arrangements.

Ultimately, the decision of whether a payday loan or an installment loan is suitable for you is a personal one. However, like any form of credit, it’s crucial to be well-informed about your own credit history, understand your affordability limits, and conduct thorough research on loan options before initiating any applications. If you seek a hassle-free process for obtaining quick cash, Wise Loan is worth considering.

The recommendations contained in this article are designed for informational purposes only. Essential Lending DBA Wise Loan does not guarantee the accuracy of the information provided in this article; is not responsible for any errors, omissions, or misrepresentations; and is not responsible for the consequences of any decisions or actions taken as a result of the information provided above.