Building a strong credit history is essential, even if you’re starting from a poor credit score. When faced with emergencies or burdened by credit card debt, bad credit loans can be a useful option. These loans often offer lower interest rates compared to credit cards or payday loans, providing some relief when better alternatives are scarce.

Let us guide you through understanding how bad credit is determined and how you can secure a bad credit loan with reasonable interest rates, utilizing your current financial situation.

Understanding Bad Credit:

Your creditworthiness is typically assessed based on your FICO score, managed by one or more major credit bureaus. The most significant factors influencing your score are your payment history and credit utilization ratio, which can change rapidly. To manage late payments that may be affecting your FICO score, consolidating debts with a personal loan can be beneficial.

FICO scores are usually categorized as Excellent, Good, Fair, and Bad. Although some variations exist among creditors, generally, bad credit is considered to be in the range of 300 – 668. Once your credit falls into this range, finding loans without high-interest rates can be challenging.

Obtaining a Loan with a 500 or Lower Credit Score:

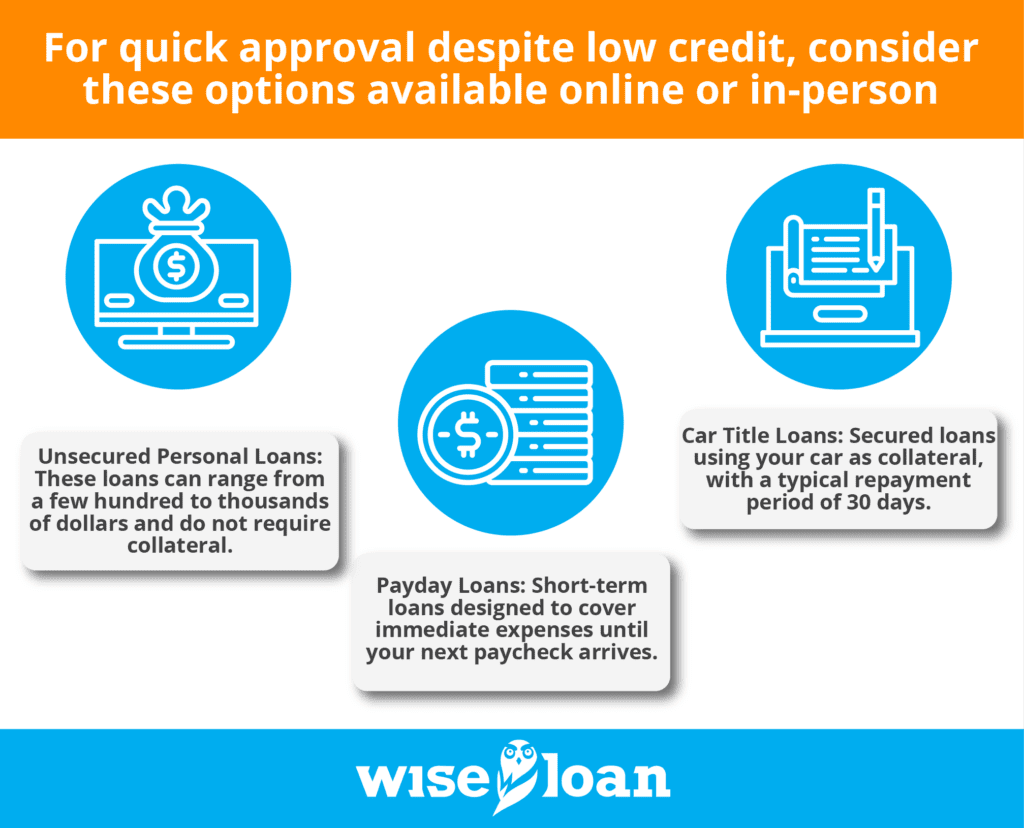

Securing a bank loan with a credit score of 500 or lower can be exceedingly difficult. However, there are alternative options to explore, each with its implications regarding interest rates, approval speed, and funding time. For quick approval despite low credit, consider these options available online or in-person:

- Unsecured Personal Loans: These loans can range from a few hundred to thousands of dollars and do not require collateral.

- Payday Loans: Short-term loans designed to cover immediate expenses until your next paycheck arrives (typically ranging from $200 to $2000).

- Car Title Loans: Secured loans using your car as collateral, with a typical repayment period of 30 days.

Choosing the Best Loan Company for Bad Credit:

Choosing the Best Loan Company for Bad Credit:

When seeking quick cash for emergencies, researching various lenders is crucial to find the best rates in your area. The internet makes this process simpler, but focus on these critical aspects:

- Quick Guaranteed Funds: Some lenders offer approval and funds within 24 hours, while others may take longer. Be prepared for your financial needs accordingly.

- Transparent Terms: Look for loans with clear and easy-to-understand terms, including APRs and fee policies, to avoid unexpected charges.

- Supportive Customer Service: Great service means having your questions promptly answered, ensuring you receive the necessary advice and assistance.

At Wise Loan, we prioritize our clients and offer reliable services and quick turnaround rates for loan applications. If you’re interested in exploring your options based on your current situation, take a moment to fill out our online application today.

The recommendations contained in this article are designed for informational purposes only. Essential Lending DBA Wise Loan does not guarantee the accuracy of the information provided in this article; is not responsible for any errors, omissions, or misrepresentations; and is not responsible for the consequences of any decisions or actions taken as a result of the information provided above.

More information on Installment Loans and how they work in your state: