If you are currently receiving disability benefits from the federal government, you might be curious about your eligibility for obtaining a loan. Specifically, you may wonder if it’s possible to get a payday loan while on disability. The answer is yes, it’s possible, but there are important details to understand before applying.

Below, we’ll explore how payday loans and other personal loan options work for people receiving disability income, including SSI or SSDI, and what to consider before borrowing.

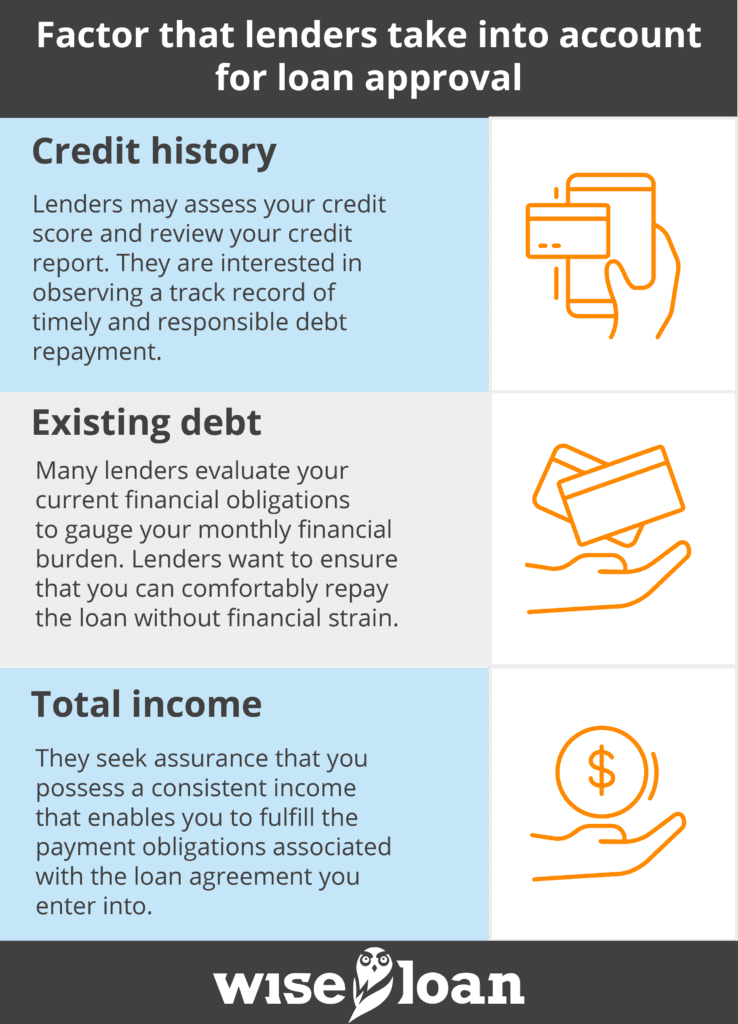

How can I borrow money while on disability?

In most cases, the requirements for qualifying for a personal loan while on disability are similar to those for individuals who are not on disability. Lenders typically focus on your ability to repay the loan rather than your disability status.

When reviewing your application, lenders may consider factors such as:

- Steady monthly income (from SSI, SSDI, or other sources)

- Banking history or account activity

- Outstanding debts or repayment history

- Loan amount and repayment term

Is disability considered income for a loan?

Indeed, disability payments are generally recognized as income when determining eligibility for a loan. Notably, Fannie Mae and Freddie Mac, the agencies responsible for establishing guidelines and regulations regarding conventional mortgages, have explicitly stated in their guidelines that disability income can be utilized to assist individuals in qualifying for a mortgage.

I’m on Social Security or disability. Can I still get a payday loan or cash advance?

Certain payday loan lenders offer cash advance loans or payday loans that are based on the amount of your SSDI benefit payments instead of a conventional paycheck. This approach allows you to obtain a loan by leveraging the value of your SSDI benefits. In this process, the payday lender arranges for automatic debits from your checking account to repay the loan, usually scheduled for the day of or after your SSDI deposit is received.

Can you get a payday loan with a Direct Express Card?

Receiving federal benefits payments through a Direct Express Card is not uncommon, as not everyone utilizes a traditional checking account for this purpose. If you happen to receive your disability or SSDI payments through a Direct Express Card, you may be able to locate a payday loan lender who is willing to accommodate payments made via this card.

Is a Payday Loan Your Best Option?

During times of financial hardship, individuals often consider payday loans due to the lenient credit check process employed by these lenders. However, there are alternative loan options available that do not require a credit check or a strong credit history. These alternatives may offer more manageable repayment terms compared to payday loans.

If you’re receiving disability or SSI benefits, a personal installment loan may be a safer, more flexible option. Wise Loan offers installment loans designed for people with limited or fixed income. These loans provide:

- Higher loan amounts than typical payday loans

- Affordable installment payments spread over time

- Credit-building benefits when payments are made on schedule

With Wise Loan, repayment fits more easily into your monthly budget rather than requiring full repayment after your next benefit deposit.

How do you build credit while on disability?

Building credit while on disability follows the same principles as improving credit at any other time. There are several actions you can take to strengthen your credit profile while on disability:

- Timely bill payments: Paying your bills promptly significantly contributes to a positive payment history, which can greatly enhance your credit score. Ensure that you make all your debt payments on time. If possible, collaborate with lenders who report payments to the credit bureaus. Wise Loan, for instance, reports payments to two of the three major credit bureaus, making it convenient to establish credit with one of our loans.

- Debt reduction: When feasible, strive to reduce the amount of debt you owe. This practice not only has a positive impact on your credit score but also enhances your eligibility for future loans. Lenders are more likely to be confident in granting loans if they see that you are not excessively burdened by existing debt obligations.

- Responsible credit card usage: It is advisable not to max out your credit cards, as high credit utilization can lower your credit score. Credit utilization refers to the ratio of your current balances to your credit limits. For example, if you have a credit limit of $1,000 and a balance of $500, your credit utilization rate is 50%. Ideally, aim to maintain a utilization rate below 30% to ensure a healthy credit profile.

Why This Matters

If you rely on disability or SSI benefits, unexpected expenses can feel overwhelming. Understanding your borrowing options helps you avoid predatory payday loans that charge high fees and short repayment terms. Choosing a transparent, installment-based lender can help you stay financially stable and even build credit over time.

At Wise Loan, we’re committed to helping people on disability and fixed incomes find fair, transparent lending options. Our online installment loans are designed to make borrowing simple, safe, and stress-free, without the hidden fees or high interest rates common with payday lenders. Apply today and see how easy it is to get the support you need.

Frequently Asked Questions

What does Direct Express emergency cash entail?

Direct Express emergency cash provides individuals with a means to access up to $1,000 of their government benefits funds even without their Direct Express card. For instance, if you misplace your card and need to request a replacement, the process can take an average of two weeks. During this period, you may lack access to the funds received from disability or SSDI. Direct Express emergency cash allows you to have these funds deposited into an account where you can readily access them.

Is it possible to obtain a cash advance while on disability?

Yes, it is possible to secure a cash advance from a lender if you are on disability. However, to proceed with this option, you would need to agree to repay the advance using a portion of your future disability payments.

How can I manage debt while on disability?

Managing debt with a limited income can pose challenges, but it is certainly feasible. Here are some tips to consider:

- Consolidation loan: Explore the option of obtaining a consolidation loan to pay off higher-interest debts. This approach can make your debt more manageable by combining multiple debts into a single payment.

- Avoid incurring new debt: Take measures to prevent accumulating additional debt, such as refraining from increasing credit card balances or taking on new loans.

- Reduce expenses: Whenever possible, aim to cut down on expenses. This will free up more money to allocate towards debt repayment.

- Pay more than the minimum: Strive to pay more than the minimum balance required on your debts, even if it’s just an additional $10 per month. Every extra payment helps in reducing the overall debt burden.

Disclosure:

The recommendations contained in this article are designed for informational purposes only. Wise Loan does not guarantee the accuracy of the information provided in this article; is not responsible for any errors, omissions, or misrepresentations; and is not responsible for the consequences of any decisions or actions taken as a result of the information provided above.

More information on Installment Loans and how they work in your state: