Are you indebted to the IRS?

Dealing with the IRS can be quite intimidating, especially if you find yourself in a situation where you owe them money on your tax return. The IRS wields considerable authority over our financial matters, and this can be quite nerve-wracking when faced with a payment requirement. Thankfully, there are numerous alternatives available aside from resorting to bankruptcy when you find yourself in debt to the IRS.

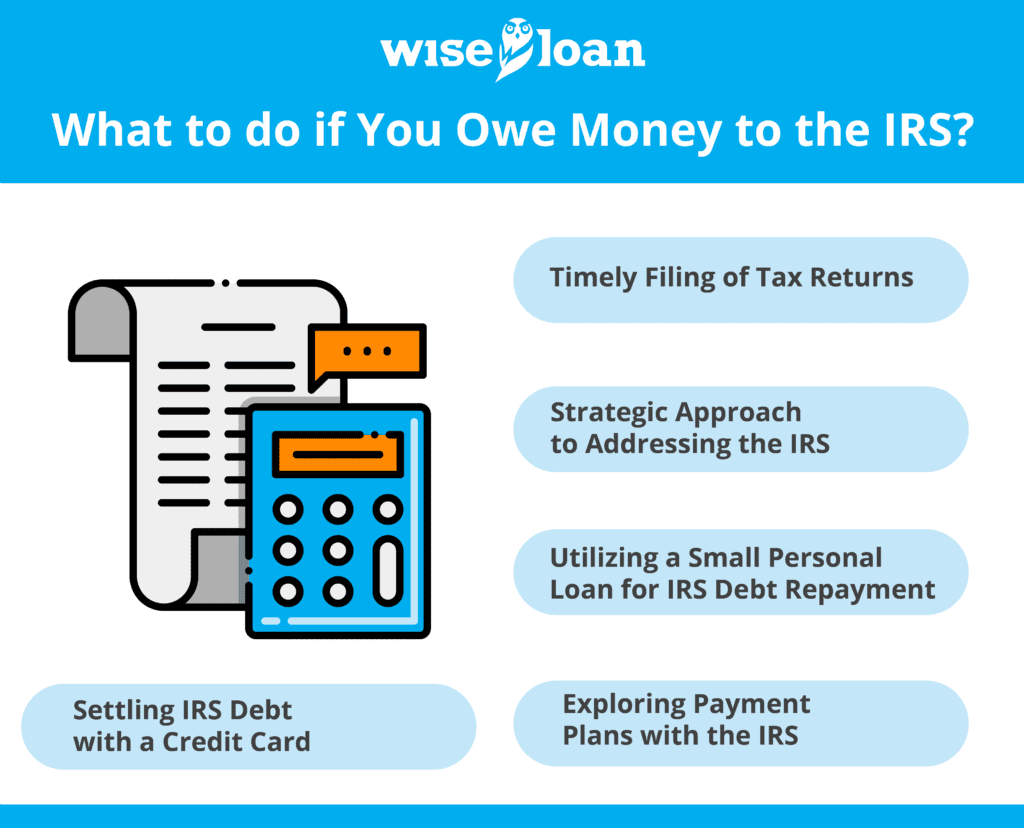

Timely Filing of Tax Returns

When faced with an outstanding debt to the IRS, the initial step is to ensure that you file your tax return punctually. Failure to file your tax return prior to the deadline, coupled with a debt to the IRS, will result in an additional 5% monthly interest charge on the unpaid balance. The IRS can impose a penalty interest rate of up to 25%. Given this, it’s unquestionably prudent to file your taxes on time, even if you owe money. The subsequent course of action is to settle your tax debt. However, in a scenario where you’ve filed your return but not paid your taxes, the IRS will levy a penalty equal to 0.5% of the unpaid amount each month. Additionally, the IRS enforces an interest rate of 3% atop the federal short-term interest rate, resulting in a combined interest rate of around 4% on the owed amount.

Strategic Approach to Addressing the IRS

Allowing your taxes to remain unpaid is akin to borrowing on a short-term basis from the IRS, and this can sometimes be rather costly. If your debt to the IRS remains outstanding for an extended period, they will initiate immediate financial actions, potentially leading to wage garnishment – whereby the IRS intercepts funds from your paycheck prior to your receipt. This is also known as wage garnishment. The IRS also retains the authority to seize your assets as a form of payment or to place a lien on your properties. A property with a lien cannot be sold without settling the IRS debt first, and such liens are automatically recorded on your credit report. Tax liens represent one of the most detrimental entries on your credit report. It’s generally less stressful to settle your tax debt than to allow it to accumulate. If you lack the immediate means to clear your IRS debt, several options are available: securing a short-term personal loan, using a credit card, or establishing a payment plan through the IRS.

Utilizing a Small Personal Loan for IRS Debt Repayment

Opting for a short-term personal loan to settle your IRS debt can be a sound decision. The loan’s interest rate is likely to be lower than the combined interest and penalty rate imposed by the IRS. Moreover, a higher credit score can translate to a more favorable interest rate on the loan. One key advantage of a personal loan is that it safeguards you from wage garnishment, tax liens on your property, or asset liquidation. However, consistent monthly loan payments are essential to avoid landing in a financial predicament.

Settling IRS Debt with a Credit Card

Using your credit card to repay your IRS tax debt can offer rewards, such as cashback or travel bonuses, especially if you employ a rewards-based credit card. Nevertheless, this approach comes with the drawback of processing fees. Failing to clear the credit card balance by the due date could result in an interest rate higher than that of a personal loan. Processing fees generally range from 1.87% to 2.25%. It’s important to note that utilizing a credit card may elevate your debt utilization ratio – the comparison of your credit card balance to your overall credit limit – a critical factor in your credit score calculation.

Exploring Payment Plans with the IRS

A third option involves pursuing a payment plan directly through the IRS. The IRS extends the option of up to 120 additional days for eligible taxpayers to settle their full owed amounts. Requesting an installment plan allows you to make regular monthly payments to the IRS. Opting for such a plan entails a fee of $43. Should your tax debt place you in a position where meeting basic living expenses becomes a challenge, you might qualify for a deferred payment arrangement. However, all IRS-offered payment plans are subject to associated fees and interest.

While owing money to the IRS can be an anxiety-inducing situation, it’s important to remember that there are strategies available to help you navigate it more effectively. Prioritize establishing a solid plan that aligns with your financial circumstances to mitigate the potential severe repercussions of IRS debt.

The recommendations contained in this article are designed for informational purposes only. Essential Lending DBA Wise Loan does not guarantee the accuracy of the information provided in this article; is not responsible for any errors, omissions, or misrepresentations; and is not responsible for the consequences of any decisions or actions taken as a result of the information provided above.