Wise Loan provides installment loans designed to help you establish credit while offering the funds necessary to address unexpected expenses or emergencies. Even if your credit score is not ideal, Wise Loan enables you to access the cash you require. While numerous payday loan options are advertised in a similar fashion, it’s important to understand the distinctions between a Wise Loan and a payday loan. Why should you opt for one over the other? Continue reading to learn more.

What Is the Difference Between a Loan and a Payday Loan?

A payday loan, also known as a payday advance, cash advance loan, or salary loan, is a short-term borrowing option where the borrower repays the loan on their next payday. When taking out a payday loan, the borrower is required to repay the borrowed amount along with a fee. For instance, if you borrow $200 from a payday loan company that charges $20 for every $100 borrowed, the total repayment would be $240.

Typically, payday loan lenders mandate the establishment of an automatic payment arrangement from the borrower’s checking account. They deposit the loan amount electronically into the checking account and automatically withdraw the repayment funds at the agreed-upon time.

In contrast to traditional installment loans, payday loans differ in their repayment terms. With an installment loan, you do not repay the borrowed amount plus fees in one lump sum with your next paycheck. Instead, you make repayments over time, including both the borrowed amount and interest, in a series of installments. The frequency of installments, whether weekly, biweekly, or monthly, depends on the terms agreed upon with the lender.

What Is Better: a Payday Loan or an Installment Loan?

Opting for online installment loans, like those offered by Wise Loan, is generally a preferable choice over payday loans. Here are several reasons why you might consider an installment loan when seeking short-term funds for unexpected expenses:

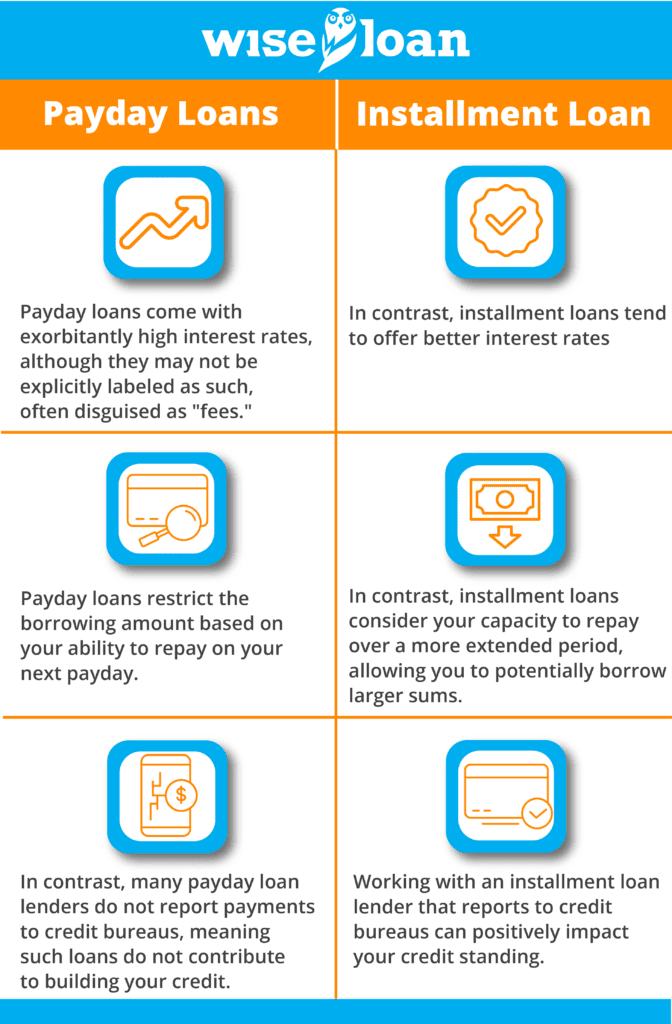

- Potentially more favorable interest rates: Payday loans come with exorbitantly high-interest rates, although they may not be explicitly labeled as such, often disguised as “fees.” When you’re charged $10 to $30 for every hundred dollars borrowed, with a requirement to repay within a few weeks, the resulting interest rate can surpass 600%. In contrast, installment loans tend to offer better interest rates.

- Access to higher loan amounts: Payday loans restrict the borrowing amount based on your ability to repay on your next payday. This limitation prevents you from borrowing the full extent of your paycheck. In contrast, installment loans consider your capacity to repay over a more extended period, allowing you to potentially borrow larger sums.

- Credit-building potential: Working with an installment loan lender that reports to credit bureaus can positively impact your credit standing. By making timely repayments, you establish a solid payment history, subsequently boosting your credit score. In contrast, many payday loan lenders do not report payments to credit bureaus, meaning such loans do not contribute to building your credit.

In summary, selecting an online installment loan offers the advantages of potentially better interest rates, access to higher loan amounts, and the opportunity to improve your credit profile.

Are Payday Loans Easier or Harder to Pay Back Than Installment Loans?

Paying back payday loans can be challenging due to the significant portion they deduct from your next paycheck. If you depend on a payday loan to cover your expenses, it can further strain your upcoming paycheck. This puts you at risk of facing financial difficulties once again in just a few weeks, as you need to allocate those funds to repay the loan.

On the other hand, installment loans involve smaller payments spread out over an extended duration. This repayment structure enables you to settle the debt without immediately burdening your finances in the upcoming weeks.

Why Should You Avoid Payday Loans?

The payday loan trap ensnares many individuals when they initially borrow funds for an unexpected expense, fully intending to repay the loan on their upcoming payday. However, unforeseen circumstances arise, and they find themselves in a situation where their entire next paycheck is necessary to cover essential expenses.

To address this predicament, numerous payday loan companies allow borrowers to roll over their existing loan into a new one, deferring repayment until the subsequent payday. However, this convenience comes at a cost. Rollover fees are imposed, increasing the total amount to be repaid and augmenting the interest on the loan. Consequently, paying back the loan becomes even more challenging, potentially leading to significant financial difficulties within your personal budget.

The Wise Loan Difference

At Wise Loan, our focus is on offering responsible lending solutions that not only provide access to necessary funds but also pave the way for a more successful financial future. With our loan products, having a great credit score is not a requirement to qualify.

Our installment loans are designed to be repaid over several months, allowing for easier integration into your budget. Additionally, we provide a range of resources to assist you in repaying the loan promptly, which can contribute to improving your credit score. We believe in rewarding your efforts towards responsible repayment.

When faced with an urgent or unplanned expense that demands immediate cash, we encourage you to consider a loan from Wise Loan rather than a conventional payday loan. You can conveniently apply online within minutes to determine your eligibility.

Frequently Asked Questions

What are two types of payday loans?

Payday loan companies offer a variety of options, including:

- Paycheck advance loans: These loans are secured based on your upcoming paycheck. On your payday, the lender deducts the loan amount directly from your bank account.

- Post-dated check loans: With this type of loan, you write a check for a future date to cover the loan amount and any associated fees. The lender provides you with the funds immediately and cashes the check on the agreed-upon date.

What is considered a payday loan?

The term “payday loan” encompasses a broad range of loan solutions. Some loans from Wise Loan may even be referred to as payday loans. However, in most cases, when people mention a “payday loan,” they are referring to a loan of $500 or less that must be repaid on or before the next payday, typically within a few weeks or a single month.

Does Wise Loan report to credit bureaus?

Yes, Wise Loan reports payments to two of the three major credit bureaus. Our aim is to assist customers in building their credit. By making timely payments on your Wise Loan, you can be confident that your positive payment history will be added to your credit report.

The recommendations contained in this article are designed for informational purposes only. Essential Lending DBA Wise Loan does not guarantee the accuracy of the information provided in this article; is not responsible for any errors, omissions, or misrepresentations; and is not responsible for the consequences of any decisions or actions taken as a result of the information provided above.

More information on Installment Loans and how they work in your state: